Friday Flyer: Italian Term Premia and Bank Share Prices: the effect of QE

After the UK referendum and the US presidential election result, there were significant movements in asset prices. Notably in the UK, the exchange rate fell by some 15% and, surprisingly in the immediate aftermath, term premia also fell by some 20Bp. But following the recent Italian referendum result and the announcement of the resignation of the Italian Prime Minister on December 4, although Italian term premia have been volatile, there has been little overall change in premia. For example, the two day change in term premia from 5 to 7 December was around 2Bp. I suggest that one reason for the relative stability is the ECB's QE programme which is providing support for bond prices with respect to changes in risk.

Authors

After the UK referendum and the US presidential election result, there were significant movements in asset prices. Notably in the UK, the exchange rate fell by some 15% and, surprisingly in the immediate aftermath, term premia also fell by some 20Bp. But following the recent Italian referendum result and the announcement of the resignation of the Italian Prime Minister on December 4, although Italian term premia have been volatile, there has been little overall change in premia. For example, the two day change in term premia from 5 to 7 December was around 2Bp. I suggest that one reason for the relative stability is the ECB’s QE programme which is providing support for bond prices with respect to changes in risk.

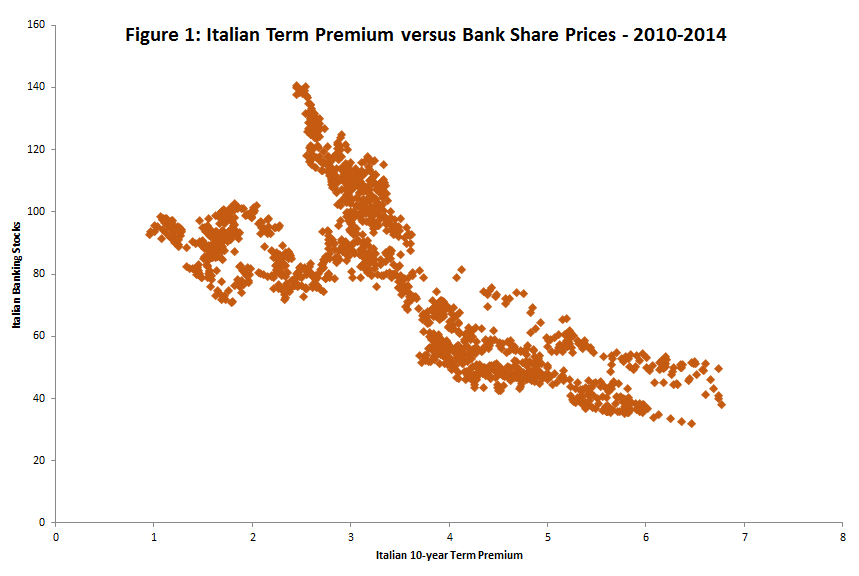

At the Institute we are able to decompose bond yields into expected interest rates, which are risk-neutral, and a term that reflects risk.[1] It is admittedly a lumpy term as it conflates liquidity, credit and term premia into one expression. Naturally we are looking at ways to decompose risk further. One way we proceed is to look at the determinants of the term premia. For Italy we can see from Figure 1 that from 2010-2014 the Italian bank share index and the estimated term premium were negatively correlated. Without making a case for causality, the Figure suggests that when the term premia were high Italian bank share prices were low and vice versa. Why might that be?

.PNG)

Well Italian bonds are claims on future Italian tax payer revenue and increased term premia indicate that the uncertainty over that future income stream is such that investors require an extra return to hold the claim. Bank share prices are essentially the discounted price of expected future profits but analogously in the case of the same profit stream but in the presence of more perceived risk, the price will tend to fall, implying that an investor will pay less for a risky profit stream than a less risky profit stream even if the cash return is the same. We can therefore expect increases in risk to lead to higher term premia and lower equity prices.

But in the case of many banks there is also a direct link. This is because banks themselves hold government bonds on their balance sheets. Italian banks hold some 22% of outstanding Italian debt and some 24% is also held by other financial institutions. This means that a perceived increase in the risk of Italian government debt directly affects the sustainability of the Italian financial sector. Furthermore if, in the event of a sustained question mark on sustainability, the financial sector were to need to recapitalisation from the state and the state’s fiscal position was thought of as risky or unsustainable itself, the recapitalisation may not be possible from claims on future Italian tax payers alone. So in effect the Siamese twins of the state and banking sector face joint peril.

And yet since 2015 when the ECB started its programme of QE the link between bank share prices and term premia seems to have broken down. In so far, see Figure 2, as when we look at changes in share prices they are no longer reflected in term premia changes. The most recent example being the aftermath of last week’s referendum result. We will do some more work to see if other factors or measures of bank risk may still stand, as we ought not to believe a simple scatter is anything more than a start of our investigations. But one compelling idea is that the ECB buying bonds under its QE programme has limited the sensitivity of premia to economic news. That is good in the sense that it is cheaper to issue debt than it might otherwise be but perhaps not so good in the sense that there is less incentive to correct underlying structural problems because the central bank is distorting market signals. That said central bank actions always distort market signals when they have traction on financial prices but the idea is to smooth the adjustment from one equilibrium to the other and if the other equilibrium involves a more stable financial sector it may be very hard to tell yet whether that adjustment has been achieved.

[1]Chadha, J. S., S. P. Lloyd, and J. Meaning (2017), Euro Area Sovereign Bond Premia: Common Risk and Safety, NIESR Discussion Paper, forthcoming.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum