Outlook and risks for the US economy

The February 2017 National Institute Economic Review discusses the possible consequences for the US economy of the significant changes in economic policy promised by the new US administration.

Authors

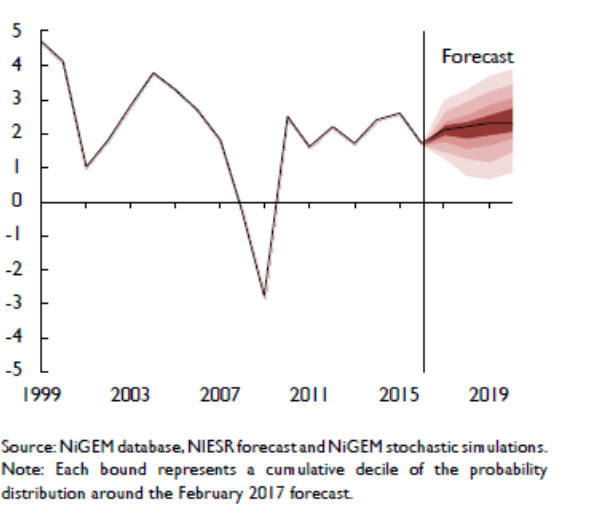

The February 2017 National Institute Economic Review discusses the possible consequences for the US economy of the significant changes in economic policy promised by the new US administration. Much remains unclear about the potential policy changes, and our baseline forecast assumes, as usual, the maintenance of existing policies: it does not incorporate any assumptions about policy changes. This adds to the risks around the baseline forecast for the US, which is illustrated in Fig 1 by the error bounds around the modal forecast for annual GDP growth. In 2017, for example, where our baseline forecast of US GDP growth is 2.1 per cent, there is a non-zero probability of growth reaching as high as 3.0 per cent or as low as 1.3 per cent this year.

Figure 1. US: GDP growth fan chart (per cent per annum)

Significant changes seem likely in several areas of economic policy, including fiscal and trade policies.

With regard to fiscal policy, President Trump has set out a “pro-growth tax plan” together with plans for increased infrastructure spending and a steady reduction of non-defence, non-safety-net spending. These potential changes suggest risks on both the upside and the downside of our growth forecast. On the upside, there may be a significant and beneficial boost to US demand growth in the short term, and also longer–term supply–side benefits if potential output is raised by productive infrastructure investment or improved tax incentives. The fiscal boost could also advance the normalisation of monetary policy and allow official interest rates to be raised to levels where their use as a counter–cyclical tool in the event of a recession again became feasible. Even this upside scenario, however, carries concerns. It would be likely to involve a significant further appreciation of the US dollar and widening of the external current account deficit, which would conflict with the new administration’s objectives of improving the US trade position and boosting manufacturing production and employment. It could therefore further intensify protectionist pressures. Moreover, while there is still uncertainty about the degree of slack remaining in the economy, recent indicators, especially the upturn in wage increases, suggest that some capacity constraints are beginning to bite. In these circumstances, a fiscal boost might not only crowd out private domestic demand and net exports through increases in interest rates and currency appreciation, but also give rise to inflationary pressure and increased inflation, especially if the new administration acts to limit the Fed’s independence.

On the downside, the envisaged changes in fiscal policy could lead to a widening of the budget deficit with little benefit to aggregate demand or productive potential if, for example, the changes are dominated by tax reductions for the wealthy and tax credits for private investors as a means of boosting infrastructure investment. In any event, because of legislative and other delays, any fiscal boost could take time and not materialise until 2018. In the meantime, demand may be constrained by the increases in interest rates and dollar appreciation that occur in anticipation of the fiscal boost, including the market movements that have already occurred. The pace of the Fed’s tightening may then need to be moderated to take account of the fact that financial markets have done some of any needed tightening for it.

Turning to President Trump’s “America–First Trade Policy”, the risks to US and global growth are clearly on the downside. Protectionist or defensive trade policies raise domestic costs and prices, thus reducing real incomes of consumers, damage economic efficiency and productivity growth by weakening competitive forces, and risk a downward international spiral of economic activity through successive retaliatory measures. President Trump has threatened to impose taxes on imports, particularly from China and Mexico and certain US companies producing abroad for export to the US. An alternative, but related, approach being considered is the introduction of a border tax adjustment to corporate income tax. All such proposals seem intended to reduce the US current account deficit and thus boost US economic growth. But achievement of this objective would be likely to be frustrated by the real appreciation of the US dollar that the trade policies would tend to cause. Since a country’s current account deficit is, by definition, the difference between its domestic saving and investment, a tariff or border tax adjustment will reduce the deficit only to the extent that it increases domestic saving (by reducing the fiscal deficit or increasing private sector saving) or reduces domestic investment. If, then, the achievement of the objective is frustrated – perhaps as the current account deficit widens on account of tax cuts and a growing fiscal deficit – additional, misconceived protectionist measures by the US could follow, exacerbating the situation.

You can find the full February 2017 National Institute Economic Review here.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum