CPI Inflation, July 2021

CPI inflation fell by a large amount (0.5%) and is now at 2.0%. All of this effect was due to the “base effect” of the spike in inflation last year (June-July 2020) dropping out. There was no new inflation in June-July 2021 as the general level of prices remained constant. The reduction in inflation was spread across most sectors, the only exception being Transport, which showed a large month on month increase, largely due to motor fuels and second- hand car prices. Clothing and footwear also showed a significant decrease due to the July sales.

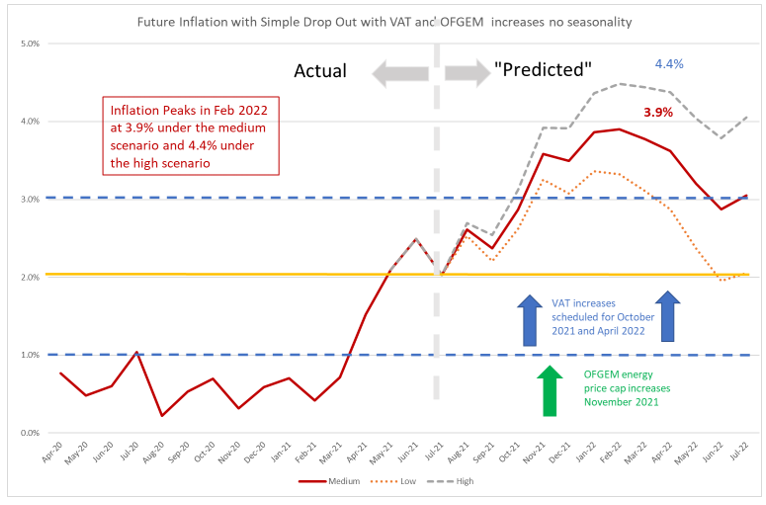

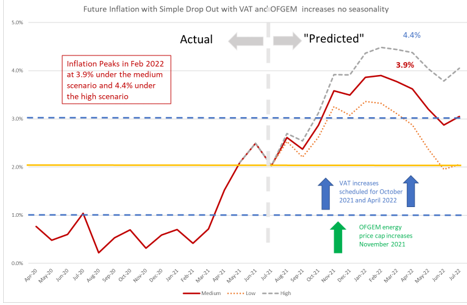

Looking forward, when we allow for the reversal of VAT reductions in the hospitality sector and scheduled rise in household energy prices announced by OFGEM, we expect inflation to increase rapidly in the later months of 2021 reaching a peak of 3.9% or higher in the first quarter of 2022, falling to about 3% by July 2022.

Authors

Main points

- The CPI inflation rate was 2.0% in June 2021, down from 2.5% in June. This decrease of -0.5% was due to the old inflation dropping out (May-June 2020), often referred to as a “base effect”. There was no new inflation between June and July 2021, with the price index remaining constant.

- The new monthly inflation rate for June-July of 0% follows on after three successive months of high monthly inflation (at 0.5-0.6% for March-April, April-May and May-June). Next month the base effect will operate in the opposite direction as the fall in inflation in July-August 2020 drops-out and will contribute a 0.4% addition to the August headline inflation (which will of course also include the additional new inflation for July-August 2021).

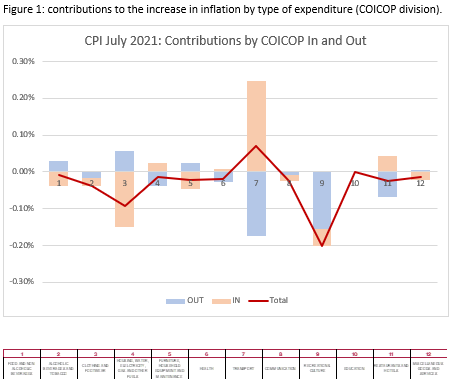

- Looking at different types of expenditure, the main contributors to the change in inflation in May-June were:

- Recreation and Culture -0.2%

- Transport +0.07%

- Clothing and Footwear, which contributed -0.09%

Negative contributions to inflation were spread across all types of expenditure except for Transport.

The contribution of each type of expenditure is measured by the sum of the monthly inflation “dropping in” and “dropping out” for the type of expenditure multiplied by the weight of the expenditure type in the CPI index. The dropping in reflects the current months new inflation, and the dropping out the inflation from May-June 2020.

In Figure 1 we see for all twelve COICOP expenditure categories used in CPI the dropping in shaded light brown and the dropping out shaded light blue with the total given by the Mauve Line. The case of Transport is interesting: the new inflation June-July 2021 was and added 0.24% to the headline, but the base effect of June-July dropping out was negative and almost as large (-0.17%) and so the overall impact on inflation was more modest at just 0.07%. In Recreation and Culture, the dropping in and out worked in the same direction to give the overall downward effect on headline inflation of -0.2%. As we can see, except for Transport, there was a tendency of inflation to fall across all types of expenditure, resulting from a mixture of old inflation dropping out and new inflation dropping in. Apart from Transport, there was positive new inflation in only three categories, and even there it made a very small contribution to headline inflation.

Extreme Items

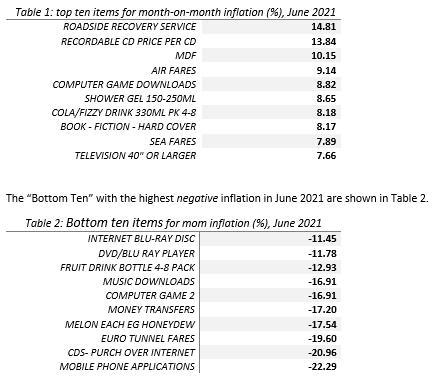

Out of over 700 types of goods and services sampled by the ONS, and there is a great diversity in how their prices behave. Each month some go up and some go down. Looking at the extremes, for this month the Top ten items with the highest monthly inflation are:

In both these tables we look at how much the item price-index for July 2021 has increased since June 2021, expressed as a percentage. These calculations were made by my PhD student at Cardiff, Yang Li.

Looking ahead

We can look ahead over the next 12 months to see how inflation might evolve as the recent inflation “drops out” as we move forward month by month. Each month, the new inflation enters into the annual figure and the old inflation from the same month in the previous year “drops out”.[1]

We do this under three scenarios.

- The “medium” scenario assumes that the new inflation each month is equivalent to what would give us 2% per annum – 0.17% pcm -(which is both the Bank of England’s target and the long-run average for the last 25 years)

- The “high” scenario assumes that the new inflation each month is equivalent to 3% per annum (0.25% pcm)

- The “low” scenario equivalent to 1% per annum – (0.08% pcm).

In addition, we also have additional “drop ins” resulting from government policy:

- The reversal of the July 2020 reduction of VAT to only 5% for hospitality, hotel and holiday accommodation and admission to certain attractions. This reversal will happen in two equal increases of 7.5% at the end of October 2021 and March 2022 returning VAT to the standard rate of 20%. These two increases will show up in the November 2021 and April 2022 inflation figures. Using the relevant CPI weights, if all the increase is passed on, the impact on headline inflation could be over 0.5% both times. However, 100% “pass through” is unlikely, and I have opted for 0.3% impact in each of the two months.

- OFGEM have announced the increase in the energy price-cap that will show up in the November 2021 inflation figures. Again, using the relevant CPI weights this gives a likely impact of 0.4%.

The patterns of the projections are similar, with big falls in September and December 2021 (as the big increases of 2020 drop out) and big increases in August (as the big fall of August 2020 associated with Eat out to Help out drops out). There is a big fall in April to June 2022 as the big increases of these months in 2021 drop out, with inflation dropping to 2.9% in the medium scenario. This fall is partly reversed in July 2022 as this month’s decrease drops out, taking the medium projection back above 3% and well away from the Bank of England’s target of 2%.

Figure 2: Looking forward to July 2022.

Commentary

After three months of high monthly inflation, we saw it drop to zero (-0.02%) in June-July 2021. The base effect of June-July 2020 dropping out lead to the big fall in headline CPI inflation of -0.5% to 2.0%, bang on the Bank of England’s target rate. However, the base effect will operate in the opposite direction in August as the fall in inflation from July-August 2020 associated with “Eat out to Help Out” drops out which will boost inflation for August 2021 by 0.4%.

In the coming months, in addition to base rate effects, there are also coming changes to government policy that will boost inflation. There is the reversal of the VAT reductions in the hospitality sector which will lead to increases in the October 2021 and April 2022 inflation figures and the increase in the household price-cap by the regulator OFGEM in November 2021.

The high levels of mom inflation in April-June 2021 will “drop out” in April-June 2022, a total negative impact on inflation of -1.6%. Thus the most likely month for a peak in inflation is February 2022.

As we go forward, higher levels of “new” inflation may be driven by a range of factors, but the most important are:

- Adjustments and supply shortages. There have been many rapid changes and adjustments made during the pandemic, which can give rise to additional costs and disruptions to supply chains. These will continue for some months but will eventually be resolved. The shortages and disruptions to container shipments, however, are taking longer to resolve than thought.

- Labour market adjustments. Patterns of employment are changing rapidly and these take time to happen (people need to move across industries, retrain etc.). Also, Furlough has kept people out of the labour market and delayed their adjustment to new market conditions. Habits have changed and people may take time to adjust their working behaviour back to the “new normal”. Brexit continues to have its effect, particularly in those sectors relying on EU nationals who have not come back since the pandemic restrictions eased.

The first of these factors can be expected to be purely transitory. Commodity prices are rising fast, but again they are not high by historic standards. Also, more importantly, commodity prices represent only a small proportion of the value-added in final consumption for many consumer goods and services. Labour market effects may also be transitory, but may persist if there is a longer-term reduction in labour supply and participation rates resulting from changes in household preferences and the resultant decision to consume less and take more leisure (in effect, the labour supply may contract and the “natural rate” of output and employment fall). The persistence of the pandemic and Brexit effect on EU labour is harder to judge, but it shows little sign of easing this year.

For further analysis of current and future prospects for inflation in the UK see:

Will Inflation take off in the UK? The Economics Observatory.

UK Economic Outlook Summer 2021: Emerging from the Shadow of Covid-19.

[1] This analysis makes the approximation that the annual inflation rate equals the sum of the twelve month-on-month inflation rates. This approximation ignores “compounding” and is only valid when the inflation rates are low. At current levels of inflation, the approximation works well, being accurate to within one decimal place of percentage annual inflation.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum