Euro area reform: implications for long-term interest rates

A previous blog discussed the implications for government bond yields of changes to euro area monetary policy, namely a reduction of assets purchased by the European Central Bank. However, this is unlikely to be the only development that will affect long-term interest rates European governments pay on their debt, and ultimately firms pay to fund investment. A second development, which may be taken into account by financial markets, is the intensifying debate about institutional reforms in the euro area.

Authors

A previous blog discussed the implications for government bond yields of changes to euro area monetary policy, namely a reduction of assets purchased by the European Central Bank. However, this is unlikely to be the only development that will affect long-term interest rates European governments pay on their debt, and ultimately firms pay to fund investment. A second development, which may be taken into account by financial markets, is the intensifying debate about institutional reforms in the euro area.

A number of ideas on how to further develop the eurozone governance framework have been floated by the European Commission, the new French president, the German government and others. These include a more powerful banking union to break the negative feedback loop between sovereigns and banks, a finance minister for the euro area, possibly with the responsibility over a common budget, a macroeconomic stabilisation function, and a European Monetary Fund. While there are exceptions (e.g. a sovereign debt restructuring mechanism), most proposals point in one direction: euro area members are likely to engage in more risk-sharing while mutual oversight over fiscal policy is being enforced. In other words, the common currency area may look much more like a federation in the future, similar to the United States or Switzerland.

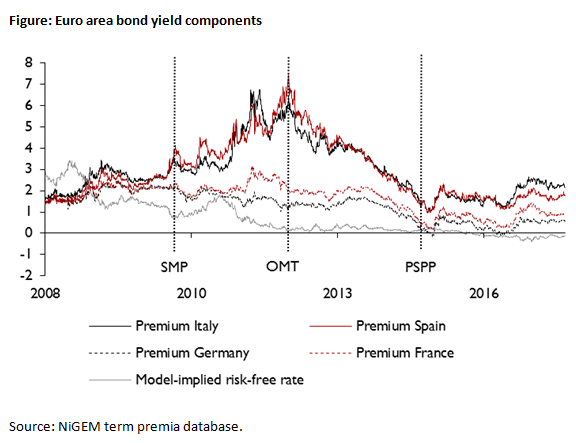

What could that mean for euro area government bond yields? Estimates of the term premium, i.e. the component of long-term bond yields that investors require as a compensation for risks such as sovereign default, reveal an interesting pattern (Figure 1). Before the European government debt crisis that started in 2010, risk premia across euro area member countries were negligible. As debt levels rose, term premia widened. But deteriorating fiscal positions cannot fully explain the divergence of Italian or Portuguese yields from their German peer. Investors’ perception of the likelihood of a sovereign default also had an important impact. Until the crisis, markets expected that financial assistance would be provided to struggling member states in the form of a bailout. As the crisis unfolded, this belief was revised and sovereign default became a possibility in the eyes of investors. Only the establishment of new institutions like the European Stability Mechanism and commitments by the European Central Bank to preserve the stability of the euro made risk premia abate.

How, then, does the institutional framework translate into risk premia? In a recently published paper, my co-authors and I try to answer this question by looking at existing federally organised countries including the United States, Switzerland, Germany and Spain. In these federations, regional governments raise part of their debt on financial markets in the form of government bonds. Yet the degree of risk-sharing varies substantially across countries, and so does the expectation that bailouts will be provided to an entity in financial difficulties (ruled out in the US, enshrined in the constitution in Germany).

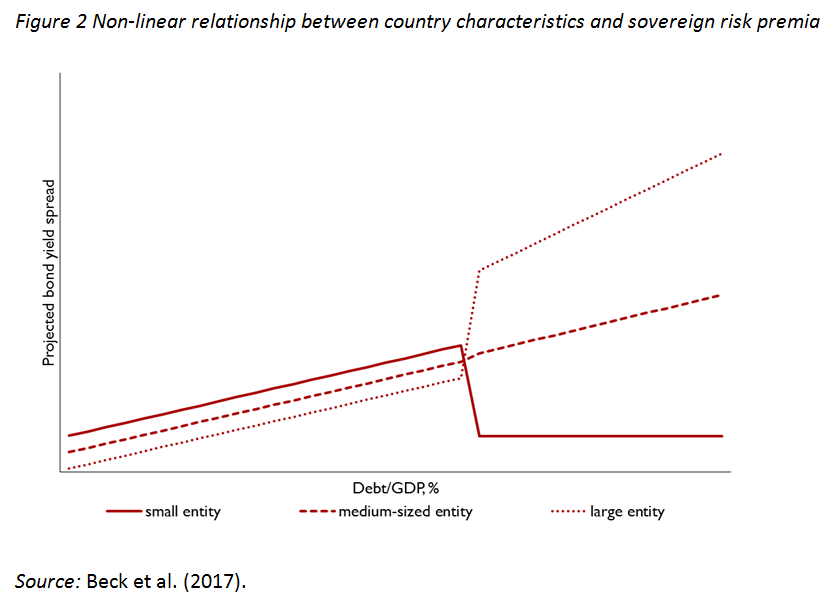

We reach three conclusions. Independent of the institutional set-up, financial markets do assess country characteristics, like debt/GDP or the fiscal deficit, when pricing government debt. However, the weight they assign to these characteristics is being reduced if risk-sharing is high and the likelihood of a bailout is large. Given a particular institutional arrangement, government entities that are relatively large within a federation pay higher risk premia for each additional percentage point of debt- or deficit-to-GDP, while smaller entities pay relatively less. Figure 2 illustrates this for a hypothetical example. For small entities the likelihood of a bailout increases after a certain threshold and financial markets require less compensation for default risk. For bigger entities, on the other hand, the capacity of the federation as a whole to provide financial assistance may not be large enough; they may be “too big to be rescued”. As a result, they are scrutinised more by financial markets and have to pay a higher risk compensation.

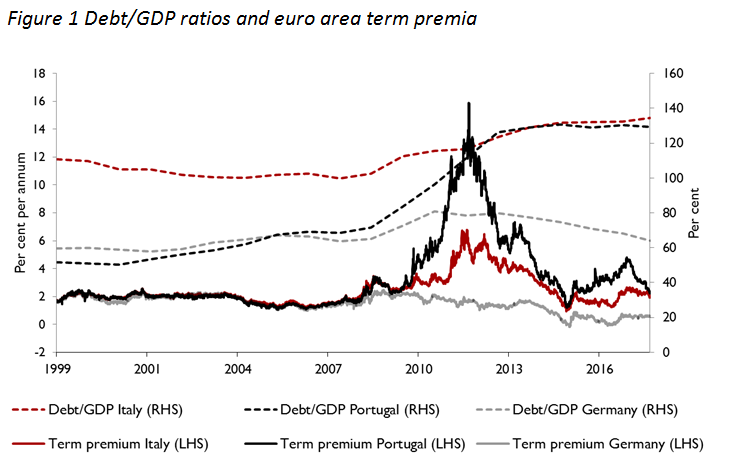

A deepening of the eurozone could therefore imply two things for euro area bond yields. As the degree of risk-sharing increases, yields are likely to converge. Yet this will probably not lead to the degree of convergence seen before the crisis and financial markets will continue to provide a mechanism to incentivise prudent fiscal policy. However, some countries may benefit more than others. Italy and Portugal currently hold about the same amount of government debt relative to GDP (Figure 1). As a large entity within the European Monetary Union, Italy may always have to pay higher risk premia for this amount of debt, holding all else equal, than Portugal.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum