Eurozone: Will a return to normal mean a return to trouble?

On Thursday, 26 October, market participants expect the European Central Bank to set out its plans for the future of its asset purchase programme. After its last Governing Council meeting, President Draghi said that the ‘bulk of decisions’ concerning quantitative easing is likely to be taken in October. What many observers wonder is: will lifting unconventional monetary policy measures lead to a renewed divergence of euro area government bond yields?

Authors

On Thursday, 26 October, market participants expect the European Central Bank to set out its plans for the future of its asset purchase programme. After its last Governing Council meeting, President Draghi said that the ‘bulk of decisions’ concerning quantitative easing is likely to be taken in October. What many observers wonder is: will lifting unconventional monetary policy measures lead to a renewed divergence of euro area government bond yields?

To gauge the response of financial markets to a withdrawal of easing policies, one needs to look at the whole package of unconventional measures taken by the European Central Bank since the financial crisis of 2008. These measures were targeted towards three main objectives:

- To respond to the dry-up of liquidity in the banking system, the ECB purchased covered bonds and provided banks with cheap credit in the form of long-term refinancing operations.

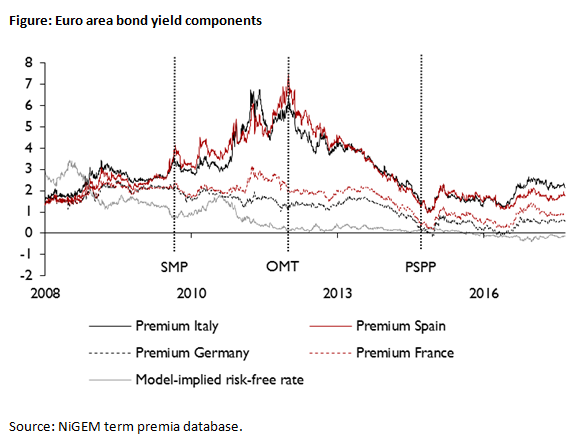

- As risks of a euro area break-up heightened and led to a divergence of bond yields across member states, the central bank took sovereign bonds on its balance sheet, first unconditionally under its Security Markets Programme (SMP), which was later on replaced by the Outright Monetary Transactions scheme (OMT). The OMT made sovereign bond purchases conditional on economic reform but has not been activated yet.

- After euro area inflation fell sharply in 2013, clearer forward guidance about the future path of interest rates was provided, deposit facility rates entered negative territory and a large-scale asset purchase programme (APP) was set up under which the ECB increased its balance sheet to more than € 4 trillion to date, buying up covered bonds, asset-backed securities, and substantial amounts of government bonds (€ 1.8 trillion).

The ECB has several options at hand to normalise monetary policy in the near term. It may focus on raising policy rates first. However, given the scepticism about quantitative easing within some (German-speaking) quarters of the system of euro area central banks, and approaching limitations to the universe of bonds to buy, the ECB has already announced its intention to sequence reductions in asset purchases before hiking short-term interest rates. Guiding expectations about both policy options can facilitate a normalisation too, as investors will be better able to price the future monetary policy stance. The ECB is therefore likely to set out a gradual plan on balance sheet reductions, with policy rate rises further out in the future.

Each policy option is likely to affect sovereign bond yields, and thereby interest rates in the wider economy, in its own way. Long-term interest rates can be broken down into a risk-free component that captures expectations about future short-term rates, and a term premium component that reflects the compensation required by investors for the risk of sovereign default or euro area break-up, for risks associated with a lack of clarity about future policy rates and liquidity risks. Monetary policy measures that change expectations about future short-term rates, like forward guidance, should mainly affect the risk-free component (signalling channel). In contrast, monetary policy measures that alleviate sovereign default and euro break-up risk will impact the premium component of interest rates (credit risk channel). Asset purchases may lead some investors to move from sovereign bonds into riskier assets, which will also affect the price of bonds and thereby the premium component (portfolio rebalancing channel).

Using NIESR’s term premia estimates, we find that the response to different monetary policy announcements by the ECB affected bond yield components quite differently. The announcements of measures targeted at reducing the risk of a euro area break-up, SMP and OMT, substantially reduced the risk premium component of those countries that were most severely affected by the European sovereign debt crisis, like Italy and Spain. By contrast, the announcement of large-scale purchases of government bonds by the European Central Bank (Public Sector Purchase Programme, PSPP) had a relatively symmetric effect on bond yields through their risk-free component, implying that the programme served mainly as a signalling device that interest rates were to remain low in the future.

A normalisation of the ECB’s unconventional policies, which may be announced as early as this Thursday, is therefore unlikely to return euro area bond markets into trouble. We expect that a gradual reduction of asset purchases combined with clear forward guidance on interest rates will not affect some euro area countries more than others. For a divergence in bond yields to happen, we would need to see a considerable return of risk associated with the stability of the euro area, for instance if reforms to the institutional framework fail to materialise or the credibility of OMT becomes questionable.