Friday Flyer: Normalising in Baby Steps

The events in the financial markets of 2007 and 2008 represented a huge economic and financial shock and the correct response was to run public deficits and to loosen monetary policy rapidly and for an extended period to facilitate as orderly an adjustment to these shocks as possible. These initial responses were intended to be temporary, as indeed are all monetary interventions. But ten years after these events, we are still running fiscal deficits and monetary policy seems ultra-accommodative.

Authors

The events in the financial markets of 2007 and 2008 represented a huge economic and financial shock and the correct response was to run public deficits and to loosen monetary policy rapidly and for an extended period to facilitate as orderly an adjustment to these shocks as possible. These initial responses were intended to be temporary, as indeed are all monetary interventions. But ten years after these events, we are still running fiscal deficits and monetary policy seems ultra-accommodative. In great part this is because advanced economies still show signs of distress. But that has not prevented a debate, given years of positive economic growth, about the case for normalising interest rates back to more recognisable levels. And in main part that is because policy rates near zero neither signal normal times nor represent anything much other than very loose monetary conditions.

The issue facing central bankers is to what extent they should respond to events and only normalise rates when the real economy has shown signs of overheating or try to pre-empt any overheating by starting the process now. It is in some sense a timeless question. Should policy be set on a backward-looking basis and respond to a clearly observed state of nature or try to be more forward-looking and respond to the perceptions of future risks? If we concentrate solely on indicators of the health of the economy, per capita real income growth and inflation by simple historical standards do not seem to justify much at all in the way of policy normalisation. But if we look at private debt levels and asset prices, there may be a clearer need to act now.

Indeed this difference between acting on risks or outcomes also plays into the debate on the role asset prices and monetary policy. Given that asset prices are forward looking claims on the value of future profits or rents, any attempt to deflate asset prices through central bank action involves a view that the central bank can better spot appropriate value than market participants. Such a contortion may be doubly hard when the market participants are themselves using central bank plans to price assets. That said, my colleague Roger Farmer has long argued that central banks should directly buy and sell risky assets to stabilise the business cycle. Indeed the extra-ordinary operations under QE may be thought of as an attempt to regulate risk.

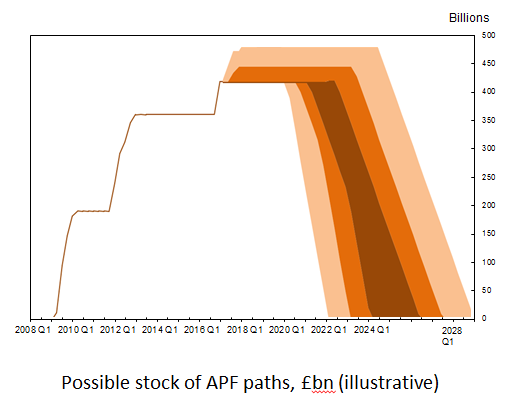

There is a further question as to whether policy should be thought of as simply the level of policy rates. Or whether we also need to examine the path of policy rates and also the extent to which any extraordinary operations will be unwound. The literature is fairly clear that all three matter. Broadly speaking, the level of rates is important for short term borrowing costs, the expected path of policy rates matters for longer term borrowing and QE may matter for both signalling about longer term rates but also in terms of affecting risk premia, which agents may otherwise pay for borrowing. If all three matter then obviously, monetary policy is now a three-clubbed tool. And we need to ask policy makers to be fairly clear about their plans for the level, the path (future changes in rates) and the stock of asset to be held.

The debate though about normalising interest rates thus is also a debate about the level, path and stock of assets held. And it is quite a lot to ask for these sets of prices and quantities to be inferred from central bank-speak alone. Under uncertainty there is a danger that markets may make incorrect inferences and so lead to excess volatility in asset prices or worse amplify the impact of any small move in policy rates. The best way to counteract uncertainty in a cycle of normalisation would be for central banks to publish the path of the policy rate, perhaps that anticipated by each voting member, and to consider moving in steps smaller that 25bp. In the August edition of the National Institute Economic Review I made a case for such an innovation. And the case still stands: in the presence of great uncertainty move slowly to your destination and plot your path with great care. We will return to this issue in our November Review, out next week. Watch this space.

.PNG)

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum