The impact of leaving the European Union is clear: what are we going to do about it?

As we have pointed out in recent editions of NIESR’s Economic Review the UK economy is showing signs of a divergence, with growth slowing here alongside growing evidence of a sustained recovery in the rest of the World.

The Referendum result and consequent uncertainty over the exact form of future trading relationships imparts two substantive effects. First, it tends to reduce expected trade in goods, capital, labour and services with the EU. Secondly, the uncertainty over future trading relationships will tend to lead to a delay in domestic investment or a diversion internationally to more certain destinations overseas.

Authors

As we have pointed out in recent editions of NIESR’s Economic Review the UK economy is showing signs of a divergence, with growth less here than the increasingly sustained recovery in the rest of the world..

The Referendum result and consequent uncertainty over the exact form of future trading relationships imparts two substantive effects. First, it tends to reduce expected trade in goods, capital, labour and services with the EU. Secondly, the uncertainty over future trading relationships will tend to lead to a delay in domestic investment or a diversion internationally to more certain destinations overseas.

The effects have imparted an asymmetric shock on the UK economy, suppressing economic activity below where it would otherwise be. The size of this shock will depend on the final trading agreement but the uncertainty is itself a source of some of the relative slowdown. Even though final exit from the EU remains some time away, the clear probability of new future trading arrangements and, relatedly, an associated slowdown in productivity growth might have acted to reduce growth now as forward-looking households and firms start to prepare for that future. Furthermore the resultant deterioration in the terms of trade reduces real income at a given level of output.

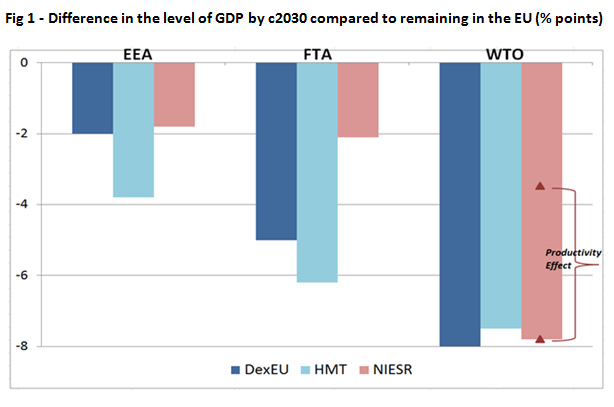

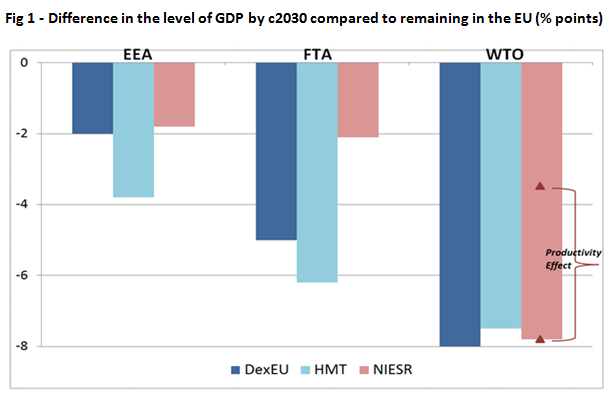

There are a number of estimates of the impact of leaving the EU on the UK economy. There is a considerable degree of consensus on the permanent impact in aggregate, ranging from some 2% of GDP in the case of a relatively benign exit involving continued membership of the EEA to some 8% of GDP in the case of exit without any form of supporting trade deal. Recent unpublished estimates from DExEU reported in the media are broadly similar to those published by HMT and the Institute in May 2016 – see Fig 1. Our estimates from prior to the Referendum included various forms of short run policy responses, with some easing in monetary and financial conditions and some support from looser fiscal policy, but they do not change the picture substantially.

The aggregate picture can be decomposed into a regional landscape showing the pockets of the country that are more or less likely to be effected from this asymmetric shock. Work published by the Institute in November suggests that in terms of the deterioration in value added the areas that trade most with the EU and in industries for which there are identifiable EU competitors will be worse hit –see Fig 2. It is entirely possible that these negative measurable effects may be offset by latent trade that we subsequently develop with other parts of the world, but the evidence to date is not convincing.

It is therefore fortunate that at the very moment that we have decided on a path of re-orienting trade, the rest of the world offers us a hand. Growth in the rest of the world seems likely to be some 4% this year and given our low exchange rate, we are able to benefit from a rather helpful degree of risk-sharing with the fruits of this higher growth, which act to offset some of the effects of trade compression. Our growth last year and this would therefore seem likely to be higher directly as a result of higher growth overseas.

The first job of the economist here is simply to measure the likely scale of trade compression and its impact on the economy. There is a literature that has done precisely that and the results are clear. But we can also understand other forces acting on the economy such as the stronger gusts of growth from overseas. In many ways the burgeoning contributions from overseas growth makes the original analysis even more convincing. Trade matters not only in the long run for growth but also in the short run. It can be disruptive and cause many short run dislocations but equally its removal or re-orientation requires careful management and nurturing of our institutional capability.

The February 2018 issue of the NIESR Economic Review is out today (7th February 2018). For the highlights of our UK forecast please read here.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum