The Lockdown Weighted Inflation CPILW For July 2020 And The Prospects For Inflation

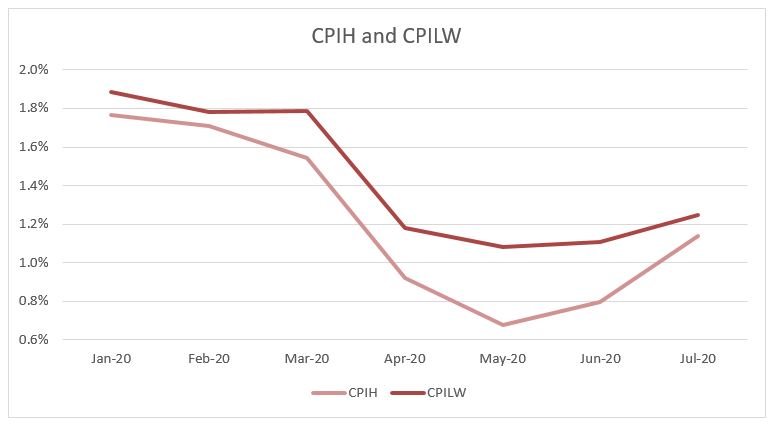

The CPIH measure of inflation has increased to 1.1% and now the gap between the lockdown measure CPILW of 1.2% is small. The use of pre-pandemic expenditure weights is no longer leading to an under-estimate of inflation.

Inflation is set to increase as the pandemic raises costs in many parts of the economy. This is unlikely to happen in 2020 as demand will remain low as unemployment and bankruptcies increase in the coming months.

Authors

The CPIH measure of inflation has increased to 1.1% and now the gap between the lockdown measure CPILW of 1.2% is small. The use of pre-pandemic expenditure weights is no longer leading to an under-estimate of inflation.

Inflation is set to increase as the pandemic raises costs in many parts of the economy. This is unlikely to happen in 2020 as demand will remain low as unemployment and bankruptcies increase in the coming months.

Whilst 2.5% is a reasonable forecast for inflation in 2021, the outturn will partly depend on how the Government and the Bank of England balance the demands of stabilising the economy and keeping public finances sustainable into the future.

.JPG)

Analysis

The CPILW for July 2020 is 1.2%, slightly up from 1.1% in June. This is only 0.1% above the official CPIH of 1.1% and indicates that the official inflation measure of CPIH no longer significantly understates inflation.

Since April 2020, the CPIH inflation figures have been constructed using the new methodology outlined by the ONS in 2020 for dealing with the effects of the Coronavirus. As discussed in this NIESR blog (Dixon, 8 May 2020), this fails to adequately take into account the changes in expenditure shares during the Lockdown. In NIESR Policy Paper 016 (April 2020), Dixon proposed a trial statistic CPILW to measure inflation using guesstimates of the Lockdown expenditure weights.

Using the Lockdown expenditure weights, the CPILW for July was 1.2%, only a slightly higher figure than the official CPIH 1.1%. The difference between the CPILW and CPIH has fallen.

The main reason for the reduced difference between CPIH and CPILW is that the annual inflation rate for Clothing and Footwear has increased from -2.1% in June 2020 to +0.1% in July. Since CPIH gave Clothing and Footwear its pre-Covid weight, this reduced the measure of inflation relative to CPILW in the months April to June. However, this effect has largely gone now which makes the two measures more similar. However, note that the increase in annual Clothing and Footwear inflation is not that clothing and footwear prices have stopped falling in July 2020. Far from it: the month on month inflation is still large, with Clothing and Footwear -0.76% cheaper than in June. The reason the annual inflation is lower is that the very big drop in prices in July 2019 has “dropped out” of the annual rate (in July 2019 Clothing and Footwear prices dropped by -2.9% in just one month).

Note that the Lockdown expenditure weights are only guesstimates and more accurate estimates will become available as data becomes available. The ONS methodology for estimating the CPIH under lockdown focussed very much on identifying “unavailable goods”. The list of unavailable goods has shrunk from over 90 in April now to just 12 in July. This means that the role of imputation of prices for unavailable goods has become insignificant for practical purposes. The expenditure shares allocated to the different categories of prices is now almost exactly the same as the pre-Covid weights.

The move to collecting all available prices online started with the April inflation figures and we now have a few months of data. What differences can we see in the prices collected? My PhD student Yang Li and I have compared the hundreds of thousands of price quotes for 2020 with the previous year. The number of prices collected fell to 66% of its 2019 figure in April and May 2020, rising to 75% in June. The proportion of price changes also fell, not in April but in May and June to 80% of the previous year. These are overall figures. If we look more closely, we see some interesting features. For Clothing and Footwear, the dispersion of prices also fell significantly with the shift to online prices, the standard deviation of prices being 60% of the previous years figure in April and May, recovering to 85% in June. This indicates that offline prices for clothing and footwear are much more variable than online. For Food and non-Alcoholic Beverages, the dispersion of prices did not change much from the previous year, as online prices for the main grocery retailers are largely the same as offline prices. Overall, if we compare RPI and CPIH, the “formula effect” does not seem to have changed much: the gap between RPI and CPIH (and CPI) remains normal. The fall in price dispersion in Clothing and Footwear does not seem to have reduced the gap via the formula effect (RPI inflation in July was 1.6%, with CPIH at 1.1% and CPI at 1.0%).

What are the prospects for inflation? Inflation is going to increase from its current low levels: the question is when and by how much? The effect of social distancing and the psychology of the pandemic are a negative “technology shock” to the service sector in particular. Even though most goods are now “available”, the expenditure patterns will remain different. Service providers such as restaurants, pubs and theatres will have to operate at low capacity with additional costs for cleaning and so on. This will result in firms going bust or closing outlets, and those that survive will increase prices as marginal costs rise. Mark-ups may fall, but the scope for a reduction in mark-ups is limited when firms are operating at low capacity. A similar story will be told in many parts of the economy.

Are there any signs of inflation picking up already? There are some. The quarterly GDP deflator for 2020 Q2 showed 6.2% quarter on quarter inflation (up from 1% in Q1). This is an annualized rate of 27%, which indicates a considerable upward pressure on prices across the whole economy. This might include “pipeline effects”

that will show through later in the year to consumer prices. However, the GDP deflator is a complex beast and involves many individual price deflators for each part of the economy and it is not easy to draw clear indications for consumer inflation from it, although the large size of the quarter on quarter GDP deflator inflation must be a cause for concern.

Looking at the “factory gate” Producer Price Index, whilst this is showing a -0.8% annual growth rate, the month on month inflation in June was 0.3% which is the largest for some time. However, the quarterly Services Producer Prices Index is still subdued: in Q2 an annual rate of 1.8%, with a quarter on quarter rate of only 0.1%.

So, the timing of the increase in inflation still looks to be late in 2020 or 2021. It is likely that the looming increase in unemployment and wave of bankruptcies will continue to keep inflation low for most of 2020 (particularly if we see a double dip recession).

As to how much inflation will rise to, this is definitely a “Fat Tail” moment: it is hard to be confident. The recent NIESR forecast of 2.5% for 2021 seems reasonable, although perhaps a little on the low side for my taste. However, the role of monetary and fiscal policy may be decisive in determining whether we might see a (much) larger figure.

Politicians will be tempted by the sirens of MMT to sustain an unsustainable deficit: who wants to cut expenditures or raise taxes? If they succumb to this temptation, then the reward will be higher inflation. This may seem alluring to some, but with near zero interest rates the effect will be one of financial repression on a large scale which, will have many unintended consequences and lead to social instability as the utility of money is degraded. To avoid this, interest rates would have to rise with inflation which could also lead to many problems in an economy as indebted as the UK. Whilst there will be many pressures on the Government to avoid the pain, I very much hope that cool heads and calm minds prevail in Numbers 10 and 11 Downing Street and we achieve the right balance between stabilising the economy in 2020 and maintaining the sustainability of public finances from 2021 onwards.

Further reading:

ONS Corona Virus and the effect on UK Prices. May 5th 2020

Huw Dixon, How can we measure consumer price inflation in a lockdown? Economics Observatory (May 25th 2020).

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum