Measuring inflation in the pandemic – June 2020

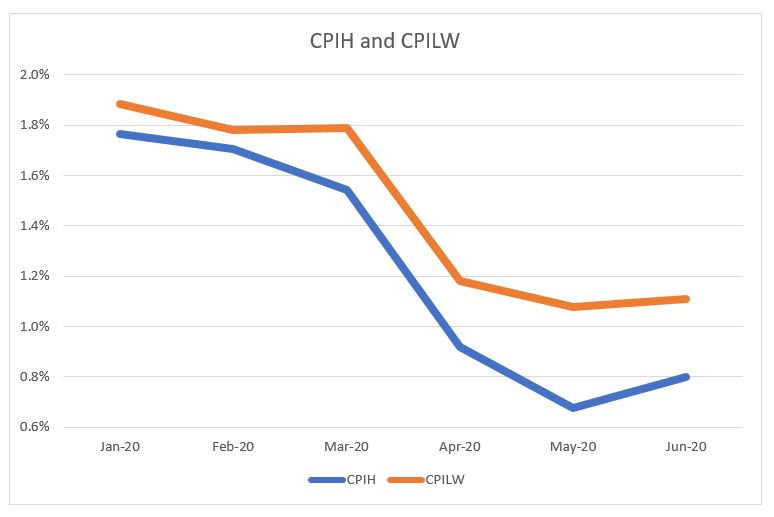

The CPILW for June 2020 is 1.1%, unchanged from 1.1% in May. This is 0.3% above the official CPIH of 0.8% and indicates that the official inflation measure CPIH understates inflation.

Authors

The CPILW for June 2020 is 1.1%, unchanged from 1.1% in May. This is 0.3% above the official CPIH of 0.8% and indicates that the official inflation measure CPIH understates inflation.

Since April 2020, the CPIH inflation figures have been constructed using the new methodology outlined ONS 2020 for dealing with the effects of the Corona Virus. As discussed in Dixon NIESR Blog 8th May, this fails to adequately take into account the changes in expenditure shares during the Lockdown. Dixon (NIESR policy paper 16, April 22nd 2020) proposed a trial statistic CPILW to measure inflation using guesstimates of the Lockdown expenditure weights.

Using the Lockdown expenditure weights, the CPILW for June was 1.1%, a higher figure than the official CPIH 0.8%. The main reason for the difference is that the CPIH keeps many expenditure weights such as clothing and footwear at pre-Covid levels and these items have on average declined by more.

The latest figures for June published this morning tell a similar story. However, the mix across different types of prices has changed. Clothing and Footwear prices are still falling, but less rapidly, with clothing and garments rising slightly compared to prices the previous month. Food and alcohol prices have also fallen from their May level. The net effect leaves CPILW unchanged: CPIH has gone up slightly. Both CPIH and CPILW are well below the CPIH figure for March of 1.5%, the last month for which the pre-Covid expenditure weights underlying CPIH were reasonably accurate.

Note that the Lockdown expenditure weights are only guesstimates and more accurate estimates will become available as data becomes available. Furthermore, as the lockdown is eased, expenditure shares will be returning towards more normal levels, so the CPILW will become closer to CPIH.

However, some changes to expenditure shares will persist: partly because of behavioural changes and partly because social distancing alters the technology of retail and services in general. Social distancing represents a negative productivity shock: the cost of selling things and providing services will increase and firms will have to raise their prices to survive as the months drag on. Since services form the bulk of the economy, this will depress productivity and the level of output for some time. Also queuing will become an established part of the shopping experiences. We know from the history of soviet economies that people want to avoid queues and be willing to pay more to go to shops where there are no queues. Again, this may lead to a separation of the market into higher priced shops for buyers willing and able to pay higher prices and cheaper shops with queues for those unable to pay more. Inflation may be low for now, but I expect many prices to rise more rapidly in the coming months.

Further Reading:

ONS Corona Virus and the effect on UK Prices. (May 5th 2020)

Huw Dixon, How can we measure consumer price inflation in a lockdown? Economics Observatory (May 25th 2020).

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum