Measuring the other half of investment

Investments in buildings, structures, transport equipment, IT hardware and other machinery make up about half of all capital expenditure by businesses in the UK. These are tangible assets – those which you can see and touch, and usually measure reasonably well. More often than not, they are bought from manufacturing companies or built by construction firms. As a result, the measurement of these investments is reasonably straightforward.

Authors

.PNG)

Investments in buildings, structures, transport equipment, IT hardware and other machinery make up about half of all capital expenditure by businesses in the UK. These are tangible assets – those which you can see and touch, and usually measure reasonably well. More often than not, they are bought from manufacturing companies or built by construction firms. As a result, the measurement of these investments is reasonably straightforward.

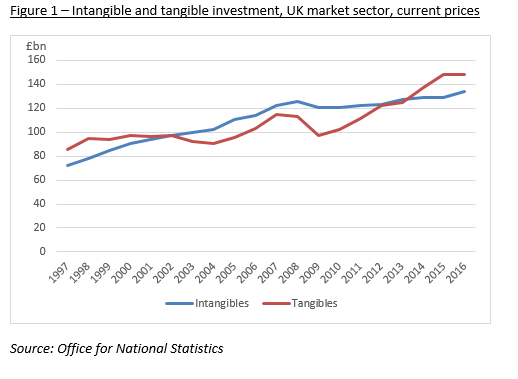

The other half of investment is in intangible assets, such as software, research and development, branding and training (Figure 1). Measuring these is far less straightforward, and the UK Office for National Statistics (ONS) have been improving the methods and data sources to do so in recent years. As well as providing improved estimates of investment for the UK National Accounts, and so for Gross Domestic Product (GDP), statistics on intangible investment also give important insights on innovation and productivity. In light of the long-standing productivity puzzle in the UK, ONS research on intangible assets contributes to an important and wide-ranging discussion on the reasons for the slowdown.

Notes: Current prices; encompass some intangible assets not capitalised in the National Accounts; market sector is whole economy excluding industries: real estate (L), public administration and defence (O), education (P), and health and social care (Q).

The broadly 50:50 split between tangible and intangible investment has held for the past two decades, but is only true when stepping beyond the National Accounts. While official measures of investment include software and research and development (R&D), among other smaller items, they exclude expenditure on market research, advertising, staff training, product and process design, and organisational improvements. Two ONS surveys on intangible investment found that the average business expected spending on these categories to provide returns over a multi-year period – the threshold for spending to be investment is that benefits exceed a year. Indeed, a growing body of academic literature supports the view that businesses make investments in these areas, and that firms that do so are more likely to perform well.

International guidance on national accounting has taken some steps to treat business spending on intangibles as investment – these changes around 2008 to treat R&D expenditure as investment. In the UK, the ONS made this change in the 2014 Blue Book (the annual comprehensive update to the National Accounts) after extensive research. The 2019 Blue Book will deliver the largest changes to intangible investment since then, improving estimates of software made in-house by businesses, and updating estimates of investment in copyrighted assets like songs, books and films.

As well as this, the ONS produces experimental statistics about the set of intangibles not treated as assets in the National Accounts. This builds on a long-series of academic work around the world, involving more people than I could name. ONS work in this area builds on this rich history, and is world-leading amongst national statistical institutes (NSIs) – few other NSIs, to my knowledge, have published statistics on intangible assets that go beyond the national accounting boundaries. ONS is also a recognised expert in the measurement of the intangible assets within the national accounting boundaries, especially for own-account software.

My paper published in the August edition of the NIESR Economic Review outlines the latest ONS research on the measurement of intangible assets in three areas: in-house branding investments, employer-funded training investments, and in-house investments in organisational capital. Over 50% of advertising is online these days, but not all of that is investment – some of it is just there to try and increase sales, but doesn’t create brand loyalty. The academic literature helps us figure out how much is really investment in a company’s brand. For branding (which covers advertising and market research), new estimates of investment made in-house by businesses are substantially higher than old ones. This suggests that in-house investment in branding is really important, and needs to be accounted for in addition to what firms spend buying these sorts of services from specialised businesses. For training, there are many surveys and data sources that ONS hasn’t used before – while ONS’ new estimates don’t make use of all of them, they make better use of them than previously, and remove some assumptions that didn’t quite work. After doing this, it looks like spending on training grew fairly consistently until about 2005, and then hasn’t changed much since – could this be a driver of the productivity puzzle?

This new research is one contribution to the growing literature on intangible assets, and the value they create in the economy. ONS research on intangibles is ongoing, providing a resource for better understanding innovation, productivity and the economy. Look out for new experimental estimates of intangible investment from the ONS early next year!

Josh Martin is Head of Intangible and Infrastructure Assets at the Office for National Statistics. His article for NIESR’s August Economic Review emerged from research presented at the ESCoE 2019 Conference on Economic Measurement. This blog was originally posted on ESCoE’s website.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum