Monday’s Macro Memo: Beliefs, Networks, History and the Housing Premium Puzzle

This is week five of my posts featuring research presented at the conference on Applications of Behavioural Economics and Multiple Equilibrium Models to Macroeconomics Policy Conference held at the Bank of England on July 3rd and 4th 2017.

Authors

This is week five of my posts featuring research presented at the conference on Applications of Behavioural Economics and Multiple Equilibrium Models to Macroeconomics Policy Conference held at the Bank of England on July 3rd and 4th 2017.

Today’s post features the coauthored work of Héctor Calvo-Pardo and a series of coauthored papers by Alan Taylor, a co-organizer of the conference.

Today’s post features the coauthored work of Héctor Calvo-Pardo and a series of coauthored papers by Alan Taylor, a co-organizer of the conference.

Hector Calvo-Pardo, from the University of Southampton presented his paper on social networks, coauthored with Luc Arrondel Research Director at CNRS in Paris, Chryssi Giannitsaro of Cambridge University and Michael Haliassos of Goethe University. Alan Taylor, a Professor at UC Davis, helped organize the conference. In a linked video, he discusses an amazing new data set developed jointly with Òscar Jordà, Vice President of the Federal Reserve Bank of San Francisco and Moritz Schularick, Professor of Economics at the University of Bonn.

Arrondel, Calvo-Pardo, Giannitsaro and Haliassos (ACGH) conduct work on social networks that fits beautifully into the theme of this conference. In the opening Macro Memo I explained how economic models with multiple equilibria could be combined with psychological models of belief propagation to advance our understanding of financial panics. The ACGH paper “Informative Social Interactions” is a very nice example of the use of network analysis to explain the propagation of ideas.

Arrondel, Calvo-Pardo, Giannitsaro and Haliassos (ACGH) conduct work on social networks that fits beautifully into the theme of this conference. In the opening Macro Memo I explained how economic models with multiple equilibria could be combined with psychological models of belief propagation to advance our understanding of financial panics. The ACGH paper “Informative Social Interactions” is a very nice example of the use of network analysis to explain the propagation of ideas.

Quoting from the paper [page 2]

“…we design, field and exploit novel survey data that provide measures of stock market participation (relative to individuals’ financial wealth), connectedness, but also of subjective expectations and perceptions of stock market returns via probabilistic elicitation techniques. Our empirical analysis exploits cross-sectional variation for a representative sample by age, asset classes and wealth of the population of France, collected in two stages, in December 2014 and May 2015.

… the questionnaire [also] contains a rich set of covariates for socioeconomic and demographic controls, preferences, constraints and access and frequency of consultation of information sources, typically absent from social network empirical studies.

And this is where networks come in:

[our data set] … contains specific questions designed to obtain quantitative measures of relevant network characteristics that enable identification of information network effects on financial decisions from individual answers…”

ACGH break up a person’s network into a small inner circle of contacts who are financially knowledgeable, and a separate larger set of contacts who are not. They find significant peer effects from contacts in the financial network to a person’s beliefs about future financial variables. The paper provides evidence of how beliefs spread through social networks, a mechanism that may help to promote the spread of asset prices bubbles. I recommend listening to Hector’s explanation in his own words, linked below.

This brings me to a fascinating series of papers by Òscar Jordà, Moritz Schularick and Alan Taylor (JST). To my knowledge, they have so far produced five papers, “When Credit Bites Back: Leverage, Business Cycles, And Crises, (2011), “Sovereigns versus Banks: Credit, Crises and Consequences” (2013), “The Great Mortgaging: Housing Finance, Crises, and Business Cycles”, (2014), “Betting the House”, (2015), and the paper I know best “The Rate of Return on Everything” (2017), which I saw presented at the NBER Summer Institute in July of 2017. This paper has two additional co-authors Katharina Knoll and Dmitry Kuvshinov who are/were both students of Moritz at the University of Bonn.

This brings me to a fascinating series of papers by Òscar Jordà, Moritz Schularick and Alan Taylor (JST). To my knowledge, they have so far produced five papers, “When Credit Bites Back: Leverage, Business Cycles, And Crises, (2011), “Sovereigns versus Banks: Credit, Crises and Consequences” (2013), “The Great Mortgaging: Housing Finance, Crises, and Business Cycles”, (2014), “Betting the House”, (2015), and the paper I know best “The Rate of Return on Everything” (2017), which I saw presented at the NBER Summer Institute in July of 2017. This paper has two additional co-authors Katharina Knoll and Dmitry Kuvshinov who are/were both students of Moritz at the University of Bonn.

The unifying theme in all of these papers is a new data set that the authors have painstakingly assembled. Here I quote from JKKST (2017):

“Our paper introduces, for the first time, a large dataset on the rates of return on all major asset classes in advanced economies, annually since 1870. Our data provide new empirical foundations of long-run macro-financial research. Along the way, we uncover new and somewhat unexpected stylized facts.

… Notably, housing wealth is on average roughly one half of national wealth in a typical economy, and can fluctuate significantly over time… But there is no previous rate of return database which contains any information on housing returns.”

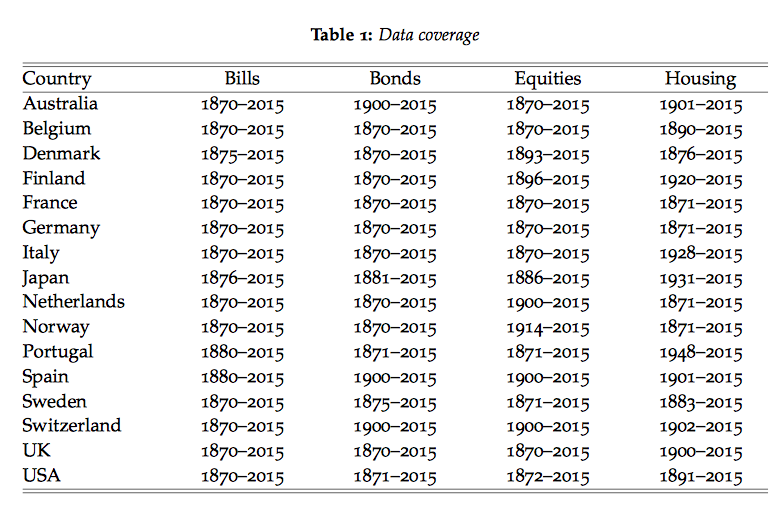

Table 1 shows the extent of the coverage which includes sixteen advanced economies for 145 years.

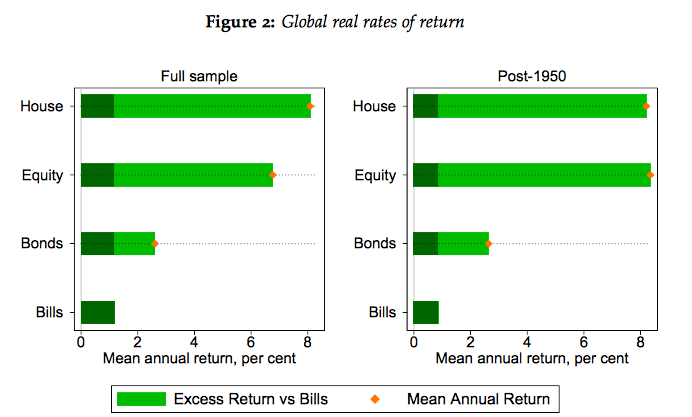

There are many nuggets to be mined here, some of which have already been dug out by the authors. For example, it is well known that the return to equity has been 5% higher than the return to T-bills in a century of US data, a fact that Rajnish Mehra and Ed Prescott labeled the equity premium puzzle. JKKST provide evidence that the equity premium puzzle is universal across all sixteen economies and, in addition, there is a second ‘housing premium puzzle’, documented in Table 2. This second puzzle is all the more intriguing since the variance of returns to housing are significantly lower than the returns to equities.

JKKST focus on the relationship between average stock market returns, “r” and average growth rates “g”. The connection between r and g has gained widespread notoriety since Thomas Piketty revived the Marxist claim that capitalism will self-destruct as the rich grow richer in his acclaimed tome, Capitalism in the 21st Century. I suggested at the recent 2017 NBER Summer Institute, that Alan and his coauthors look instead, at the connection between the safe rate of return and the growth rate. If, as I suspect, the safe rate of return is roughly equal to the growth rate across these data, it suggests (to me) that Samuelson’s biological rate of interest is at play. It’s time to start teaching our graduate students more about the Overlapping Generations Model, just one of the topics I’ll be covering in a series of ten lectures on Indeterminacy and Sunspots in Macroeconomics, as part of the Swiss Doctoral Programme at Gerzensee this week.

JKKST focus on the relationship between average stock market returns, “r” and average growth rates “g”. The connection between r and g has gained widespread notoriety since Thomas Piketty revived the Marxist claim that capitalism will self-destruct as the rich grow richer in his acclaimed tome, Capitalism in the 21st Century. I suggested at the recent 2017 NBER Summer Institute, that Alan and his coauthors look instead, at the connection between the safe rate of return and the growth rate. If, as I suspect, the safe rate of return is roughly equal to the growth rate across these data, it suggests (to me) that Samuelson’s biological rate of interest is at play. It’s time to start teaching our graduate students more about the Overlapping Generations Model, just one of the topics I’ll be covering in a series of ten lectures on Indeterminacy and Sunspots in Macroeconomics, as part of the Swiss Doctoral Programme at Gerzensee this week.

Related Blog Posts

Child Language Brokering: What It Is and How It Is Experienced By Migrant Families

29 Jan 2024

7 min read

What are the Experiences of Latin American Migrants Accessing Healthcare?

16 Oct 2023

5 min read

Related Projects

Related News

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

Thousands Of Households Projected To Face Monthly Mortgage Repayments Greater Than Their Monthly Incomes

03 Nov 2022

2 min read

Related Publications

The Nature of the Inflationary Surprise in Europe and the USA

21 Mar 2024

Discussion Papers

Supporting Immigration Advice Amidst Financial Challenges: Local Authorities’ Funding Initiatives

29 Feb 2024

Topical Briefing

Implications of the Transition from Defined Benefit to Defined Contribution Pensions in the UK

07 Feb 2024

UK Economic Outlook Box Analysis

Exploring Alternative Data Sources for Household Wealth Statistics

24 Jan 2024

Discussion Papers

Related events

Taxing Consumption