Reducing risks of financial instability in the Euro Area

In its August Review, NIESR revised its forecast for GDP growth in the Euro Area in 2017 up to 2.0 per cent from 1.6 per cent projected in May. The Review also noted that the recent significant strengthening of growth in the Area had been accompanied by a smaller divergence of growth performance among member countries than seen in most of the period since the euro was introduced.

Authors

In its August Review, NIESR revised its forecast for GDP growth in the Euro Area in 2017 up to 2.0 per cent from 1.6 per cent projected in May. The Review also noted that the recent significant strengthening of growth in the Area had been accompanied by a smaller divergence of growth performance among member countries than seen in most of the period since the euro was introduced. Alongside these welcome economic developments, the political uncertainty in Europe, which we discussed in the May Review, arising from the unusual concentration of elections, has been resolved to a significant extent by the elections in France.

However, there are still risks of financial instability in the Euro Area, arising partly from shortcomings in the institutional arrangements of the monetary union and partly from the continuing economic imbalances among member countries.

Action to complete the monetary union is behind schedule, as discussed in Box A of the August Review in the context of a recent European Commission paper on the subject. We argue that the recent strengthening of economic performance in the Area, combined with the more conducive political environment, provides an opportunity that should be grasped by the Area’s political leaders to take the action needed to complete EMU, particularly the banking union, and thus reduce the risks of further financial crises in the Area.

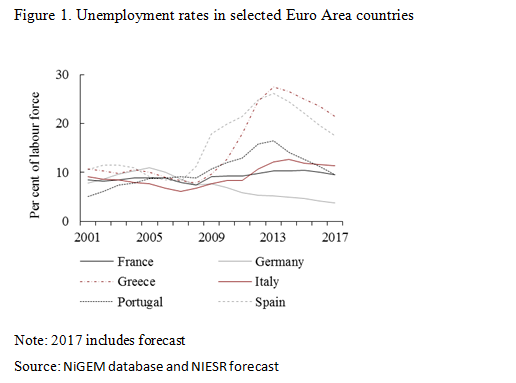

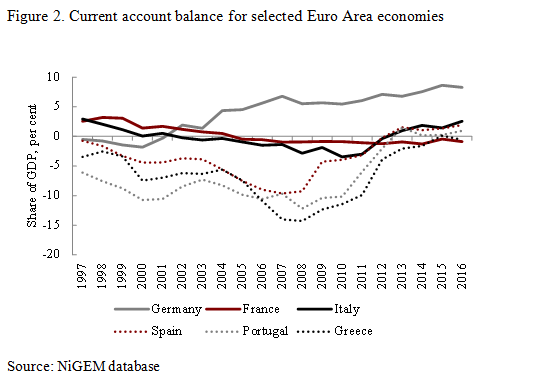

Regarding economic imbalances, among the major problems of the Euro Area from its inception in 1999 has been the divergence of cost competitiveness among member countries, and the associated divergences among unemployment rates and financial balances.

In Germany, since the introduction of the euro, unemployment has fallen from about 8 to below 4 per cent (see figure 1) while the external current account balance (see figure 2) has been transformed from a deficit of 2 per cent of GDP to a surplus of more than 8 per cent. These two developments together imply that there has been a major increase in Germany’s international competitiveness in the past 17 years. In most of the Area’s other member countries, unemployment has risen since the introduction of the euro and is very high—around 10 per cent or higher—in several cases. In the countries where unemployment is high, fiscal policy is constrained by debt levels or EU rules, or both, which means that these countries can act to reduce output gaps only by attempting to improve their international competitiveness by reducing costs. But with inflation already low, even lower inflation in these countries would make it more difficult for them to reduce their debt burdens.

Meanwhile, Germany has the largest external current account surplus in the world in absolute terms and last year had a fiscal surplus of 0.8 per cent of GDP. Wage increases are subdued, at 1.9 per cent in the year to the first quarter of 2017, and consumer price inflation, at 1.5 per cent in the year to June, is below the ECB’s target. Germany therefore has the space both to boost domestic demand through fiscal expansion—perhaps by raising the country’s relatively low infrastructure investment—and to promote larger wage increases.

Use of this space would serve several purposes. The boost to demand in Germany would promote growth in its Euro Area partners suffering high unemployment. Larger wage increases in Germany would boost the cost competitiveness of its trading partners in the Area without the deterioration of their debt burdens that lower inflation in their own economies would involve. An increase in infrastructure investment in Germany should boost the economy’s productive potential. And the reduction of Germany’s external surplus could contribute significantly to the reduction of global payments imbalances and thus reduce both the risks of instability in foreign exchange and financial markets and the risks of protectionist pressures.

Current economic and political circumstances provide an opportunity to complete the institutional arrangements of the monetary union and to address the Area’s economic imbalances, and thus to make the future economic success of the union more secure.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum