Three challenges for the French economy on the eve of a political transition

As French citizens prepare to go to poll on Sunday to elect their representatives in the National Assembly, the lower – and more powerful – of the two chambers of parliament, here is a snapshot of how the French economy has performed in the last five years, identifying three key challenges to long-term prosperity. To follow through on President Macron’s reformist agenda, it is important that a majority willing to tackle those problems emerges from the assembly.

Authors

As French citizens prepare to go to poll on Sunday to elect their representatives in the National Assembly, the lower – and more powerful – of the two chambers of parliament, here is a snapshot of how the French economy has performed in the last five years, identifying three key challenges to long-term prosperity. To follow through on President Macron’s reformist agenda, it is important that a majority willing to tackle those problems emerges from the assembly.

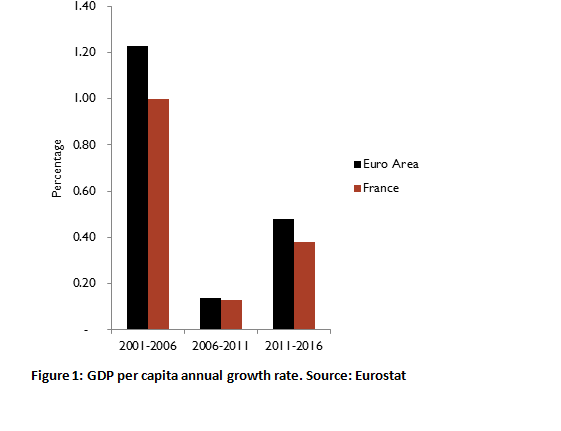

At the broadest level, the French economy under-performed in comparison with its Euro Area partners for the last five years, extending earlier trends. French GDP per capita grew between 2011 and 2016 by 0.4% per annum compared to 0.5% in the Euro Area (Figure 1), which means that French GDP per capita is now only 107% of the Euro Area average, compared to 110% in 1999 at the creation of the Euro. To reverse this trend, the new French government will need to undertake reforms to address its fiscal position, encourage job creation and to restore competitiveness.

1.Fiscal position

First, France has to restore its fiscal position back to a more sustainable path, while improving the efficiency of the public sector. The reduction of its budget deficit from 5.1% in 2011 to 3.4% of GDP in 2016 was of a smaller magnitude than the contraction achieved by other Euro Area countries, and this means that France has continued to breach the Maastricht treaty limit of 3% for the ninth consecutive year. As a result, French debt ratio to GDP has continued to increase, reaching 96.3% in 2016, in contrast with the Euro Area where the debt ratio has declined in the last two years (Figure 2). In the May edition of the National Institute Economic Review, we forecast the budget deficit to stay slightly above the Maastricht limit in 2017. Emmanuel Macron will therefore face the dilemma of either enforce his lauded European credentials by abiding by the Maastricht rule, or implement his fiscal programme presented during the campaign. Macron’s plan includes a reduction in corporate tax from 33.3% to 25%, €50bn of additional public investments and a progressive reduction in public spending reaching €60bn per year in 2023. Because tax cuts would precede reductions in public spending, we expect the plan to initially increase the budget deficit, before reducing it as the spending cuts are implemented.

2.Unemployment

One of the main challenges for the newly elected government will be to reform the labour market, so as to improve the matching efficiency between companies’ demand and labour supply. Between 2011 and 2016, unemployment increased from 9.2 to 10.1 and stayed at a high level despite policies aimed at reducing the cost of labour (Crédit d’Impôt pour la Compétitivité et l’Emploi (CICE) in 2012 and Pacte de Responsabilité et de Solidarité in 2014). For example, research by Carbonnier et al shows that CICE had no direct impact on employment, but instead increased wages and corporate profits. Now that a large portion of unemployed people have been out of work for several years, helping them find a job will be a difficult task. Recent data from INSEE show a welcome decline to 9.6% of the unemployment rate in the first quarter of 2017. But looking at the numbers in details, we find that the employment rate stays stable, which means that the decline in unemployment is the result of a reduction in the number of people actively looking for a job, and not of the economy creating more jobs. Decreasing the unemployment rate was one of the most repeated objectives of former President Hollande, and failure to do so has eroded his popularity. If Macron can successfully reform the labour market by lifting the rigidities in its microstructure, he would reap significant benefits in terms of political credibility and improved economic prospects.

3.Competitiveness

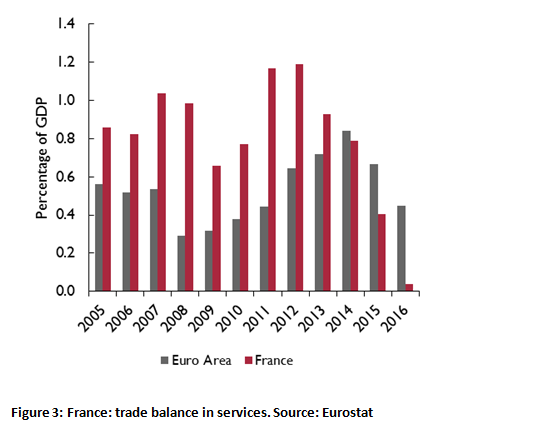

A third challenge is to improve French economy’s competitiveness, which has deteriorated recently despite targeted efforts to reduce administrative burden and labour cost. Exports have grown slower in volume between 2011 and 2016 at 3.0% per annum in France than in the Euro Area at 3.6%. Even in the service sector, which used to be one of France’s strengths, the trade surplus vanished from 1.2% of GDP in 2012 to zero in 2016 (Figure 3, for our May Review). The main components of this decline were (1) transports – with the expansion of market share of foreign low-cost airlines and Eastern-European truck delivery companies – (2) tourism, which was severely impacted by the wave of terrorist attacks in France that started in 2012 and (3) business services.

Our May 2017 forecast – which came before Macron’ election and did not take into account any of his proposed policies – was that GDP growth will increase from 1.1% in 2016 to 1.2% in 2017 and 1.4% in 2018. With this favourable backdrop, the incoming government and assembly should endeavour to reform public sector and labour market and improve competitiveness in order to put France at the forefront of European economies. If La République En Marche, Emmanuel Macron’s party, were to be the one leading these reforms – and recent polls give it an absolute majority – it would be an extraordinary achievement for a party created only one year ago.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum