Uncertainty Matters: Past, Present and Future

A fog of uncertainty has hung over the British economy since the summer of 2016. The EU referendum, snap general election and hung parliament coincided with spikes in quantitative measures of uncertainty. The Bank of England, HM Treasury and the International Monetary Fund argue that this uncertainty will not pass without economic consequences.

Authors

A fog of uncertainty has hung over the British economy since the summer of 2016. The EU referendum, snap general election and hung parliament coincided with spikes in quantitative measures of uncertainty. The Bank of England, HM Treasury and the International Monetary Fund argue that this uncertainty will not pass without economic consequences.

While it is too early to definitively test this hypothesis, history offers an interesting case study. The interwar period in Britain was also a time of heightened uncertainty and for strikingly similar reasons, such as the snap general elections of 1923 and 1931, the brief hung parliament of 1929-31 and the issue of trade barriers. As tariffs were implemented in Europe and the United States, the United Kingdom promoted a policy of imperial preference with its far-flung colonies and dominions.

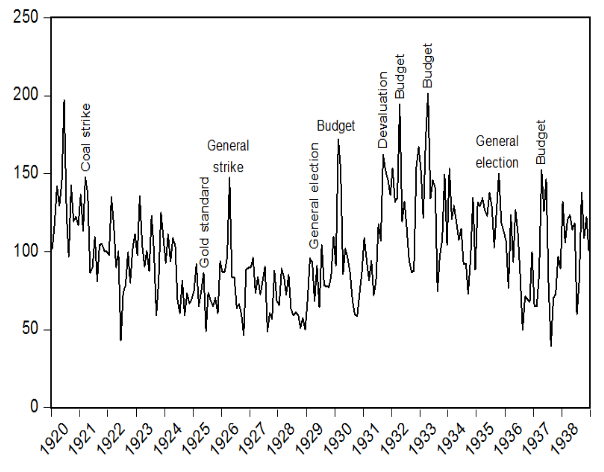

In new research, I investigated how uncertainty affected the economy in interwar Britain. As a nebulous concept, the first challenge was to measure uncertainty. Following the novel approach developed by Scott R. Baker, Nicholas Bloom and Steven J. Davis, I constructed an index based on the frequency of articles expressing uncertainty over economic policy in the Daily Mail, The Guardian and The Times. The new index is shown in figure 1.

Figure 1. Economic Policy Uncertainty in the United Kingdom, 1920-38

.PNG)

Source: Author’s calculations. The data is available from policyuncertainty.com.

The second challenge was to identify the macroeconomic effects of these fluctuations in uncertainty. Using a statistical model, I found that a major uncertainty shock reduced economic activity by 2.8 per cent, raised the unemployment rate by 2 percentage points and accounted for a fifth of macroeconomic volatility. These effects were not instant, but were felt for two years after the shock.

The depressive impact of uncertainty was not lost on contemporaries. William Morris, founder of Morris Motors Limited, stated in 1930 that Britain was “floundering in a sea of uncertainty […] the result being colossal unemployment.” In the same year, the Labour government faced a vote of no confidence on this issue. Winston Churchill appealed to the House of Commons, “the charge that we make against the Chancellor of the Exchequer is that, without due cause, he has created uncertainty which has been harmful to trade and employment.”

A century on from the interwar period, uncertainty is on the rise again but where is the fall in economic activity? While uncertainty would tend to depress the economy, the loosening of monetary policy, depreciation of sterling and recovery of world trade would tend to stimulate it. Thus, the bad and the good may have cancelled out, leaving economic growth as it stands: positive but below average in terms of its recent past and relative to other advanced countries.

As we stand between phases 1 and 2 of the Brexit negotiations, we are once again knee deep in a sea of uncertainty. Reducing this uncertainty would be politically challenging, but a cheap boost to sluggish economic growth. As Stanley Baldwin, who was Prime Minister three times between the wars, put it in 1930, “business can flourish with tariffs. Business can flourish without tariffs. Business cannot flourish where there is uncertainty.”

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum