What Can Be Done About the Cost-of-Living Crisis?

Last week, we highlighted the impact that the rising prices and higher taxes are having on household budgets. Our analysis showed that, without government intervention, about 250,000 more households will slide into destitution whilst approximately another 500,000 households face the choice between eating and heating.

Authors

In our latest UK Economic Outlook, the focus was on the substantial impact of soaring prices on low-income households. Besides the poorest who risk sliding into more debt and destitution, a striking result of our research was that 11.3 million households struggle to make ends meet because their budgets are being squeezed by wages and benefits not keeping pace with accelerating inflation and higher taxes. The policy path embarked on by the government is not helping enough to cushion the blow.

Speaking to Max Mosley and Tibor Szendrei, a PhD student at Heriot-Watt University who has worked with the NIESR team on regional and distributional analysis, Professor Adrian Pabst discussed NIESR’s approach to the cost-of-living crisis and policy options to help the hardest hit households.

Who is most affected by the cost-of-living crisis?

We know that low-income households are hit hardest by the rising prices of necessities, as products such as food and energy disproportionately dominate their household budgets. But this is just one side of the picture: incomes aren’t keeping up with prices, and in the case of some they are falling following the removal of the £20 uplift to Universal Credit. With expenditures rising and incomes falling, what many households have left over at the end of the month is getting smaller or disappearing altogether as they have to dip into their savings to pay the bills.

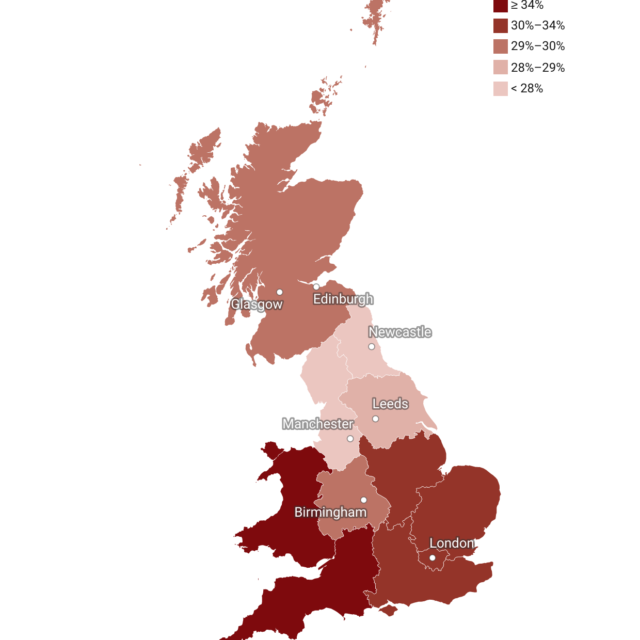

We found in our quarterly outlook that 1.5 million households (5 per cent of the population) have food and energy bills greater than their disposable income. For these households, who likely do not have sufficient savings or access to credit cards to help them cope with these prices, we can expect them to either resort to payday loans, or simply not pay their bills by going into arrears and incurring more long-term debt.

Of all the measures that capture the effect of the cost-of-living crisis, including measures of poverty and destitution, we believe that this is one of the clearest ways to identify the critical financial situation that applies to so many people across the UK, with a particular high incidence in parts of London, Scotland and Northern Ireland.

Is there anything we could do to help them?

Before suggesting policies, we need to identify precisely what we’re trying to achieve with more targeted intervention. No policy can completely compensate for the effect of inflation, as most of the price increases are driven by global economic factors. But although it is inevitable that households will see some reduction in their real income, it is not a given that this has to affect most of all the poorest households.

So instead of designing policy to offset the effect of inflation, we should attempt to make the impact more equally distributed. We identify that the lower-income households have seen their incomes fall further than the median by a total of £4.2 billion, which we use as the target for policy intervention.

We recommend that the Chancellor raises Universal Credit by £25 a week between May and October this year, which would cost £1.35 billion. He should also provide a one-off cash transfer of £250 to these poorest households which would cost a further £2.85 billion. We leave these policies for six months, as we do not know, for instance, how much the energy price cap will increase by. Because of this uncertainty we recommend a review in October to assess the situation and adjust policies accordingly.

But the government says increased spending to help these households would damage the economy. Is this the case?

The government has given two reasons for not increasing spending further: one is the effect increased public debt would have on the economy and the other is the potential inflationary consequences of giving people more cash.

Thinking about the first, the Office for Budget Responsibility (OBR) provides the government with estimates of what they call ‘fiscal headroom’, which is a measure of how much additional borrowing the government could commit to without adverse economic consequences. Before the Spring Statement, that headroom stood at £20 billion, of which the Chancellor has spent about £10 billion in his package of support announced in the March Spring Statement. We therefore suggest that if there is an additional £10 billion remaining, this should be spent on cushioning the effects that inflation is having on the poorest households.

On the concern over inflation, we have in fact modelled this scenario using our unique economic models here at NIESR. We did not find any significant effect on inflation that would be a cause for concern. This is likely because household consumption only makes up 60% of the economy, and only 5% of households would benefit from these policies. On the contrary, the households in question have a high propensity to consume, which means a high fiscal multiplier. So they would spend a very large fraction of every Pound given to them and thereby help to boost consumption and investment, which would sustain the rate of economic growth that is slowing down and worsening overall economic conditions.

Related Blog Posts

Child Language Brokering: What It Is and How It Is Experienced By Migrant Families

29 Jan 2024

7 min read

What are the Experiences of Latin American Migrants Accessing Healthcare?

16 Oct 2023

5 min read

Related Projects

Related News

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

Thousands Of Households Projected To Face Monthly Mortgage Repayments Greater Than Their Monthly Incomes

03 Nov 2022

2 min read

Related Publications

Related events