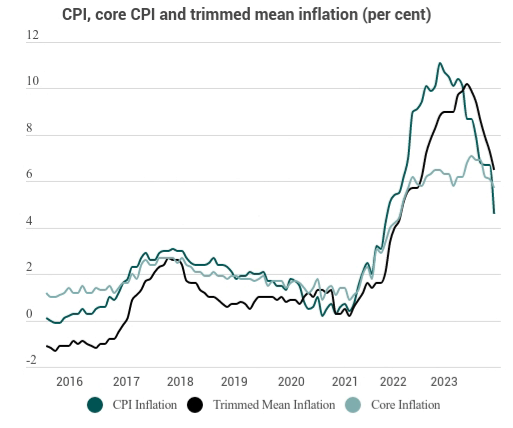

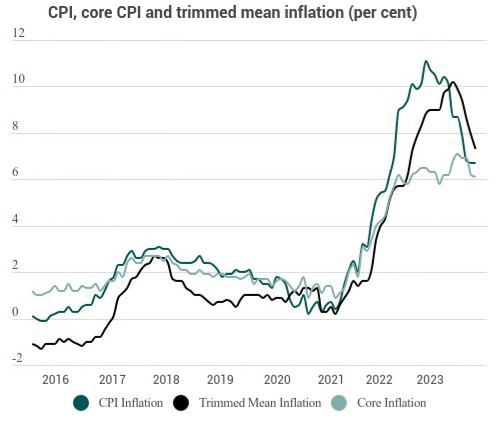

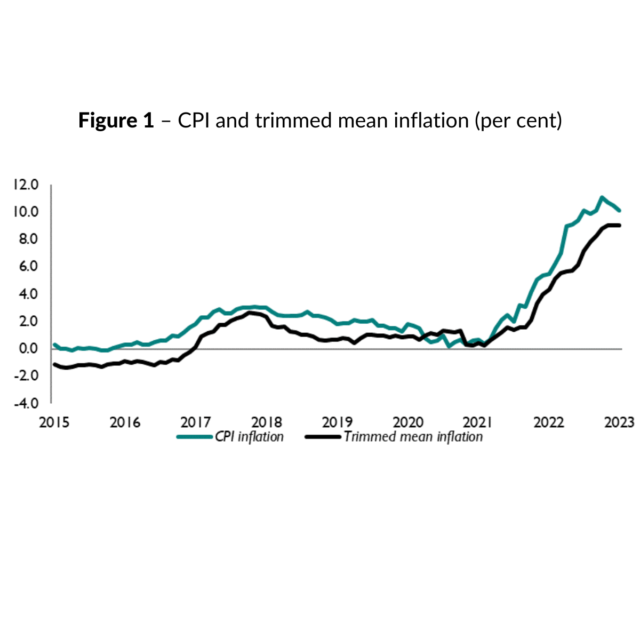

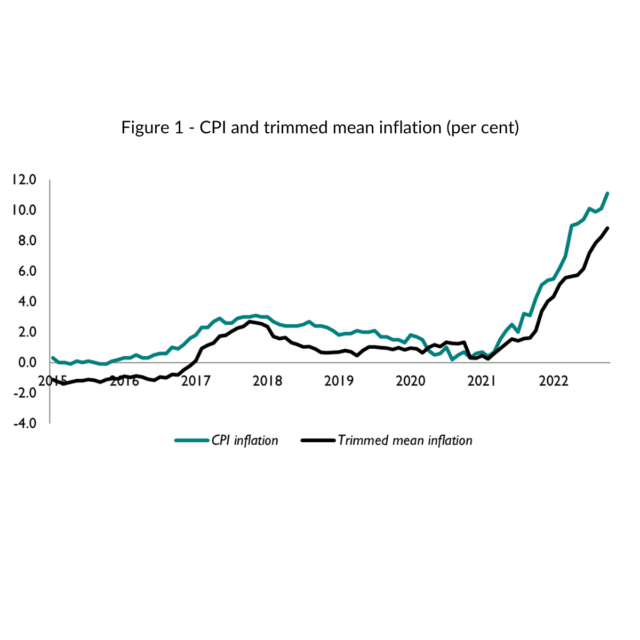

CPI Trackers

CPI inflation reflects changes in the prices of thousands of products, some of them quite volatile. Our monthly CPI Tracker looks in detail at changes in the prices of individual products to try to get a measure of underlying inflation.

Subscribe to CPI Tracker releases

Publications - all CPI Trackers filters

Inflation Holds Steady at Four Per Cent, But is Set to Fall in Coming Months

14 Feb 2024

CPI Trackers

Downward Contributions in Nearly all Categories Bring CPI to 3.9%

20 Dec 2023

CPI Trackers

CPI Holds at 6.7 per cent as Measures of Underlying Inflation Remain High

18 Oct 2023

CPI Trackers

Large Falls in Underlying Inflation Ahead of Tomorrow’s MPC Meeting

20 Sep 2023

CPI Trackers

Welcome Fall in Headline Rate Despite Little Movement in Underlying Measures

19 Jul 2023

CPI Trackers

Energy Prices Drive Fall in CPI, Masking Worrying Underlying Trends

24 May 2023

CPI Trackers

Unexpected Rise in Inflation Complicates Tomorrow’s MPC Decision

22 Mar 2023

CPI Trackers

Moderate Fall In Inflation In January Masks A Serious Fall In Real Wages

15 Feb 2023

CPI Trackers

Underlying Inflation Reaches New Record High Ahead of MPC Meeting Tomorrow

14 Dec 2022

CPI TrackersTrackers

Difficult Challenges Ahead for MPC with Underlying inflation in the UK Hitting Record High

19 Oct 2022

CPI Trackers

Although the Latest Fall in UK Inflation in August to 9.9 per cent Looks Positive, Underlying Inflation Still Remains at Record High Levels

14 Sep 2022

CPI Trackers