Press Release: Global Economic Outlook – Global Inflation fears escalate as GDP returns to its pre-pandemic level

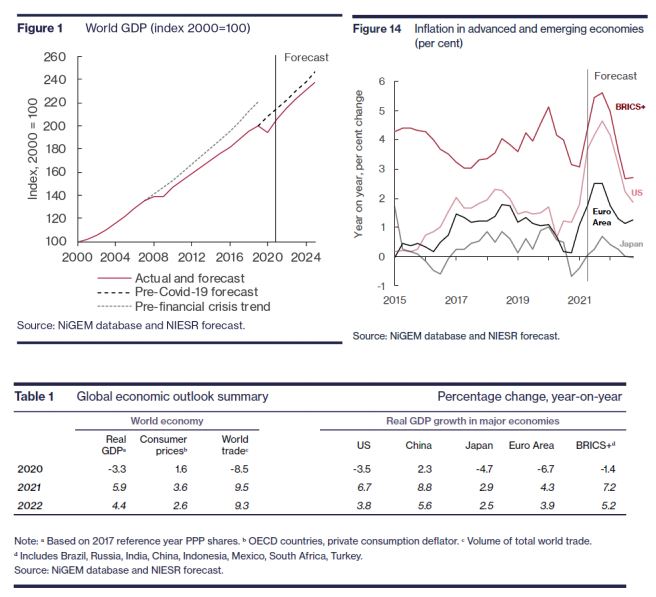

- We have raised our forecast for global GDP growth this year from 5½ per cent to almost 6 per cent, with GDP growth of 4½ per cent (up from 4¼ per cent) for 2022.

- The pace of economic recovery differs across economies. China’s GDP in the first quarter was already 8 per cent above its end-2019 level and GDP in the US has exceeded its pre-pandemic level in the second quarter of 2021. But GDP in the Euro Area has lagged is forecast to remain below its pre-pandemic level until mid-2022.

- Over the past quarter, inflation has surprised on the upside, especially in the US, with the demand boost from the American Rescue Plan, combined with other factors such as rising commodity prices and supply chain disruptions. CPI inflation at 5.3 per cent in June was the highest since July 2008. We expect that this increase in inflation will be largely temporary.

- The continued spread of the virus means that the economic outlook remains subject to considerable uncertainty. With over 4 million deaths recorded globally and new Covid-19 cases running at around 3 million a week in the first half of July, the threat to health and economic activity is far from over.

- The pace of vaccination has been uneven across countries, and there remains an imperative for international cooperation to ensure that vaccinations are widespread to low and lower-middle income countries to gain maximum benefits.

- Government support for economies and the drop in tax revenues has led to government debt to GDP ratios in advanced economies rising by around 15 – 20 percentage points, equivalent to around $7 trillion.

- Despite government interventions, we estimate that the pandemic will result in global GDP being around $4 trillion (about 2½ per cent) lower in 2025 than our pre-pandemic expectation.

- The likelihood of slower human capital growth, because of educational disruption, reduced on-the-job training and the increase in unemployment, partly explain such a longer-term economic scarring.

Corrado Macchiarelli, NIESR’s Research Manager for Global Macroeconomics, said:“Stronger GDP growth projection since the Spring is encouraging. A key issue is still the divergent experience across countries, both in economic and in health terms. The Euro Area seems to be lagging much of the rest of the advanced world. But with strong demand and supply constraints, all eyes are now on whether the increase in inflation will be temporary. If the US Federal Reserve is forced to tighten policy early, our work suggests it will hit emerging and developing economies particularly hard.”

ENDS

——————————

Notes for editors: Details of NIESR’s previous global economic forecast can be found here.

For a full copy of the world economic forecast or to arrange interviews and background briefings with our country specialists and senior researchers, please contact the NIESR Press Office: press [at] niesr.ac.uk / n.lakeland [at] niesr.ac.uk / 020 7654 1920

For technical questions related to the forecast, please contact:

- Hande Küçük on h.kucuk [at] niesr.ac.uk

- Iana Liadze on i.liadze [at] niesr.ac.uk

- Barry Naisbitt on b.naisbitt [at] niesr.ac.uk

Related News

NIESR Welcomes Delegation from Ukrainian Council for Economic Reconstruction

30 Jan 2023

2 min read

Thousands Of Households Projected To Face Monthly Mortgage Repayments Greater Than Their Monthly Incomes

03 Nov 2022

2 min read