Press Release: Second wave to cause further contraction in Q4

- The economic contraction resulting from Covid-19 and resultant public health measures has been unprecedented. The public sector has acted as a shock absorber to protect households and businesses, temporarily raising government debt levels, but the recovery has been hampered by uncertainty, repeated changes in policy, and now by the resurgence of the virus.

- The second wave of the virus, and newly announced November lockdown, are likely to further increase the fall in 2020 GDP to around 11-12 per cent. This includes a fall of around 3 per cent in the fourth quarter of 2020, with additional public borrowing but a slower rise in unemployment due to the extension of the furlough scheme.

- The end of the Brexit transition period and the prospect of a No Deal Brexit represent significant threats to the UK’s economic recovery, whether in the middle of a ‘second wave’ or after the recovery is underway. The addition of this on top of Covid-19 is likely to broaden the shock to growth and employment in the first quarter of 2021, weakening the UK’s recovery compared with other countries, and reducing productivity in the long run.

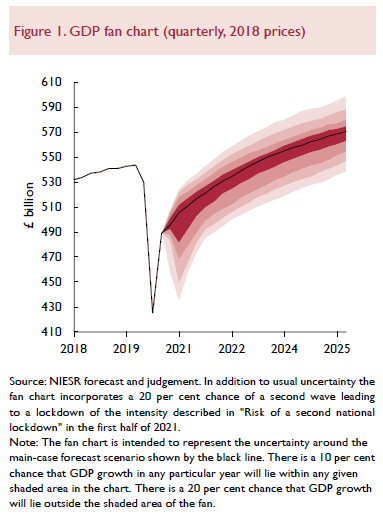

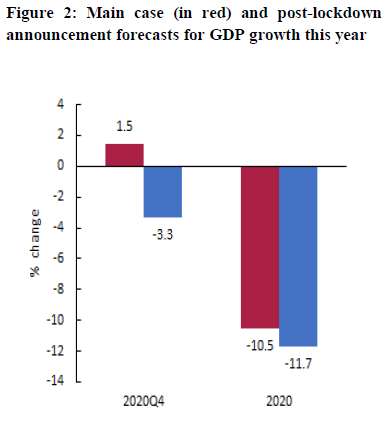

The UK economy’s recovery from the Covid-19 pandemic remains fragile and with significant risks to the downside: risks from the resurgence of the virus, from the negotiations over a trade deal with the European Union, and from the premature withdrawal of economic policy support. According to our main case GDP forecast scenario, drawn up before Saturday’s announcement, chances of a V-shaped recovery already looked to be negligible (figure 1). Saturday’s announcement of a further he November lockdown in response to resurgent Covid-19 will push growth in the fourth quarter negative, to an estimated -3.3 per cent (figure 2).

Our main case forecast scenario for 2021 and beyond was constructed to be conditional on no new national lockdowns on the scale of that seen in April being imposed, and a vaccine becoming available at some point around the middle of 2021. In that case we envisaged growth of –10.5 per cent this year and 5.9 per cent in 2021, with the 2019 fourth-quarter peak reached again in 2023.

Our main case scenario was for unemployment to rise to above 7 per cent in the final quarter of 2020 and 8 per cent in the first half of 2021 as the Coronavirus Job Retention Scheme (CJRS) ends: the extension in November will have reduced this at the end of 2020 but may just have postponed it. Unemployment is expected to rise above 5 per cent until 2024, with long-term persistent unemployment exacerbated by the prospect of a long and uncertain recovery. This would have been significantly higher had the government not already largely extended its furlough scheme in the form of the Job Support Scheme, though with reduced generosity.

“The fast-unfolding second wave, November lockdown and looming Brexit threaten the recovery. The economic outlook is extremely uncertain and depends critically on whether we win the fight against Covid-19”, said Hande Kucuk, NIESR Deputy Director.

.PNG)

ENDS

——————————

Notes for editors:

The full forecast for the UK economy will be published in the National Institute Economic Review no. 254 on Wednesday 4 November. Details of NIESR’s previous UK economic forecast can be found here.

For a full copy of the world economic forecast or to arrange interviews, please contact the NIESR Press Office: press [at] niesr.ac.uk / l.pieri [at] niesr.ac.uk / c.ridyard [at] niesr.ac.uk / 07930 544 631 / 07970 984913

For technical questions related to the forecast, please contact:

- Hande Kucuk on +44 (0)7825 642202 / h.kucuk [at] niesr.ac.uk

The National Institute Economic Review is a quarterly journal of NIESR. From this issue the NIER is published by Cambridge University Press (CUP). Founded in 1534, CUP is the world’s oldest publishing house and the second-largest university press in the world.

The Review is published in February, May, August and November, and it is available from Cambridge University Press here. For enquiries please contact: journals [at] cambridge.org

Further details of NIESR’s activities can be seen on http://www.niesr.ac.uk or by contacting enquiries [at] niesr.ac.uk Switchboard Telephone Number: +44 (0) 207 222 7665

Related Blog Posts

Related Projects

Related News

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

The Key Steps to Ensuring Normal Service is Quickly Resumed in the Economy

13 Feb 2023

4 min read

Related Publications

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

Spring 2023 Economic Forum

Winter 2023 Economic Forum

Autumn 2022 Economic Forum

Summer 2022 Economic Forum

Spring 2022 Economic Forum

Winter 2022 Economic Forum