Press Release: UK Economic Outlook – Rising inflation puts the Bank of England on the spot

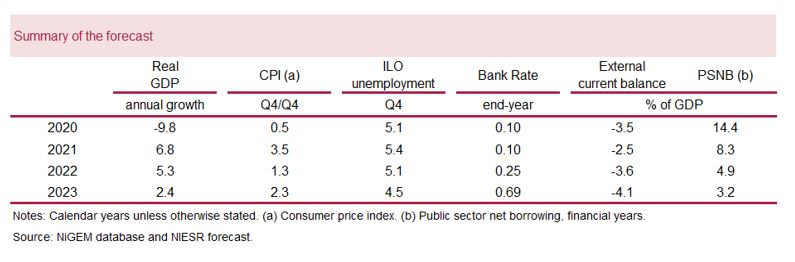

- We expect GDP to grow by 6.8 per cent in 2021, an upward revision of 1.1 percentage points since May’s Spring Outlook, and 5.3 per cent in 2022. The latest data suggest that – while headline growth and business optimism are strong – the recovery is not yet broad-based, being principally driven by the re-opening of a few sectors. Output is expected to return to its pre-Covid level in the first quarter of 2022.

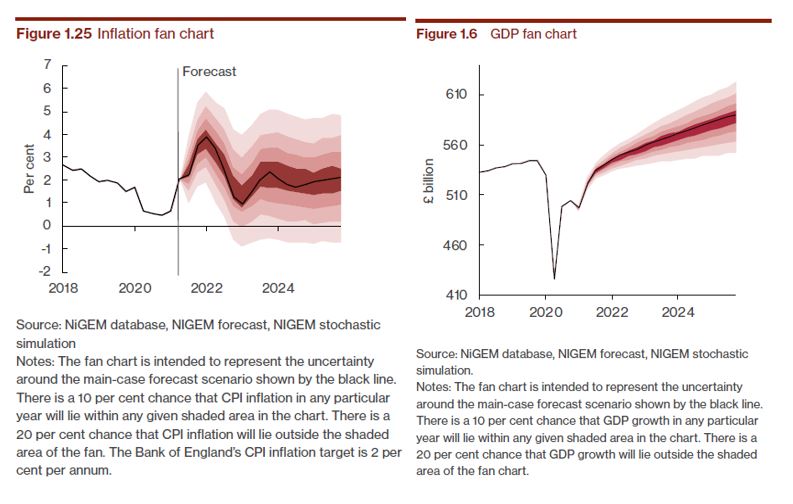

- We forecast CPI inflation to rise to 3.5 per cent in the last quarter of the year, peaking at 3.9 per cent in the first quarter of 2022 but then falling again to settle around 2 per cent in 2023. This forecast is conditional on policy rate starting to be normalised in the last quarter of next year in line with market expectations, and inflation expectations remaining well-anchored.

- The unemployment rate is now forecast to peak at 5.4 per cent in the final quarter of 2021, with most furloughed staff either returning to their existing jobs or filling the current gaps in the labour market. Following the end of the Coronavirus Job Retention Scheme, the jobless figures will see an increase of 150,000.

- Real household incomes are forecast to grow by 2.8 per cent this year after falling by 0.6 per cent in 2020: strong earnings growth, driven by the return to full earnings of furloughed staff, is partially offset by higher inflation.

- Government debt continues to rise, with borrowing for the year expected to be 8.2 per cent of GDP but is forecast to peak at 98.6 per cent of GDP next fiscal year. Debt interest payments are projected to be higher due to higher interest rate expectations, but tax receipts are higher as a result of faster growth, which also acts to reduce the ratio of debt to GDP. Additional public investment of around £30 billion per year would be consistent with stable public debt at the end of the parliament.

- We forecast growth of 14 per cent in the construction sector, bouncing back from 2020’s fall. This, and the rise of 9 per cent in private non-traded services, provide the majority of 2021’s growth. Manufacturing and private traded services, less badly affected in 2020, are forecast to grow by 6 and 5 per cent respectively this year.

- To be alert to the potential for transitory inflation effects becoming more persistent, several indicators should be monitored over the coming weeks and months: underlying wage growth after adjusting for base and compositional effects; market and household expectations for future inflation; firm mark-ups; and any sign of contagion from sectors experiencing temporarily high inflation to the rest of the economy.

- The combination of a Free Trade Agreement Brexit and Covid-19 has contributed to a forecast level of UK GDP around 3 per cent lower in the medium term than implied by the post-GFC trend. There still exists the possibility that this could be worse if downside risks materialise.

At the regional level, only the West Midlands and London are projected by the end of 2024, to have GVA about 4-5 per cent above the pre-pandemic level at the end of 2019: still only about half what growth over this period would have been in normal times.

The number of unemployed women is expected to rise across all age groups between 18 and 64 years. This also applies to young (18-24) and older men (50-64), but not men aged 25-49.

To avoid more people sliding into extreme poverty and to support consumption, we are arguing for the continuation of the Universal Credit uplift of £20 per week per household. Such a policy would cost 5% of aggregate benefit payments, and would help those most at risk from destitution.

NIESR Deputy Director, Dr Hande Kucuk, said: “Supply-side factors and effects of reopening amid the recovery in consumption are likely to keep inflation well-above the Bank of England’s 2 per cent target for the most part of next year. Now is the time for the Monetary Policy Committee to prepare the ground for normalising its monetary policy stance by clearly communicating how asset purchases and the Bank rate will be adjusted in response to a changing inflation outlook. Given the uncertainties regarding the exit from QE, the Bank should follow a carefully communicated gradual approach to avoid a significant tightening in financial conditions that might risk the ongoing recovery from the pandemic.”

ENDS

——————————

Notes for editors:

The full forecast for the UK economy can be found here. Details of NIESR’s previous UK economic forecast can be found here.

For further queries or to arrange interviews and background briefings with our country specialists and senior researchers, please contact the NIESR Press Office: press [at] niesr.ac.uk / press [at] niesr.ac.uk / n.lakeland [at] niesr.ac.uk / 020 7654 1920

For technical questions related to the forecast, please contact:

Cyrille Lenoël / c.lenoel [at] niesr.ac.uk

Rory Macqueen / r. macqueen [at] niesr.ac.uk

Hande Küçük / h.kucuk [at] niesr.ac.uk

Further details of NIESR’s activities can be seen on http://www.niesr.ac.uk or by contacting enquiries [at] niesr.ac.uk Switchboard Telephone Number: +44 (0) 20 7222 7665

Related News

NIESR Welcomes Delegation from Ukrainian Council for Economic Reconstruction

30 Jan 2023

2 min read

Thousands Of Households Projected To Face Monthly Mortgage Repayments Greater Than Their Monthly Incomes

03 Nov 2022

2 min read