Fraying at the Edges

As the war in Ukraine drags on, the human cost of this tragedy gets ever higher. At the same time, increased commodity prices and the effects of sanctions are causing additional pain to the global economy.

Sign in to Access Pub. Date

Pub. Date

03 August, 2022

Pub. Type

Pub. Type

Authors

External Authors

Summary

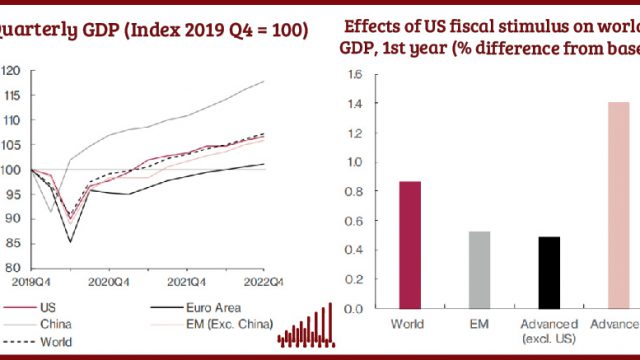

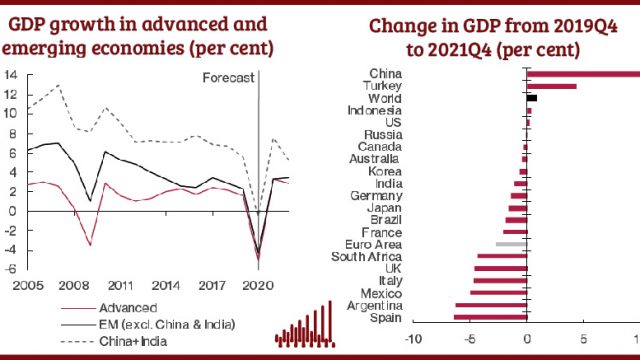

- The war in Ukraine continues to darken global economic prospects by adding inflationary pressure and increased geo-political uncertainty. The sanctions imposed on Russia, the continued supply chain disruptions, and the Chinese slowdown in response to renewed Covid-19 threats, have led us to revise down our forecast for global GDP growth from our Spring Outlook both this year and the next, from 3.3 per cent to 2.8 per cent, and from 3.2 per cent to 2.8 per cent, respectively. There are increased recession risks in a number of countries, including in the US.

- We have, in light of the latest information, raised our inflation forecast further in the current outlook. In particular, we have increased our OECD inflation forecast for 2022 from 8.2 per cent to 9.6 per cent, the highest rate since 1988, and for 2023 from 4.4 per cent to 6.2 per cent. Inflation has continued to over-shoot central banks’ expectations, especially in the advanced economies, and is expected to remain high in these economies through 2023 because price pressures have broadened beyond volatile items, such as energy. Food prices are now rising as the blockade of Black Sea ports affects the global supply of staple items such as wheat and sunflower oil.

- We continue to forecast that the pace of inflation will slow in 2023 and 2024. While the inflationary pressures coming from commodity prices remain high, the very steep rise in prices is assumed to level off as global growth slows, with higher policy and market interest rates hitting global demand. At the same time, current evidence suggests that medium-term inflation expectations remain relatively anchored. We forecast that inflation will remain elevated through 2023 but will be on a downward trend, settling at slightly above 2 per cent for most advanced economies starting from 2024.

- In light of these developments, we have seen a faster monetary tightening in the US, Canada, and the Euro Area than we expected in Spring.

- After the second consecutive 0.75 percentage point increase in July, we now assume that the US Federal Reserve (Fed) raises policy interest rates to 3.5 per cent by the end of this year and 3.75 per cent by the end of 2023. This pace of tightening should result in both a slowdown in US economic growth and inflation. The European Central Bank (ECB) has only recently given in to the pressure to increase rates, launching at the same time a new tool to avoid risks of financial fragmentation. The key uncertainty about economic activity in the Euro Area remains the possible effects of oil and gas embargos, in particular the uncertainty around Russia’s supply of gas to Germany through the Nord Stream 1 pipeline. We have explored this issue in our Risk Scenario.

- The tighter US monetary policy stance has led to higher market interest rates and an appreciation of the US dollar against most currencies, particularly among emerging economies. Those countries that are best positioned to avoid the negative effects of a US dollar appreciation are those that are commodity exporters, who will also benefit from higher commodity revenues. We continue to observe a strong divergence in economic performance between China and India, on the one hand, and other emerging economies, on the other. The war, together with US interest rates rising, is putting additional pressure on countries such as Sri Lanka, where high inflation and severe food and petrol shortages are causing the worst economic crisis since its independence. The effects of the oil shock on monetary policy in the US are explored in our NiGEM Topical Feature.

- Given the uncertainties about the duration of the war in Ukraine and the responses to higher inflation across many countries, our forecast remains subject to considerable uncertainty. Our forecast and revisions since our Spring Global Economic Outlook are summarised in Table 1.

See our Global Outlook Topical Features

You can watch our quarterly Economic Forum, where you can hear more about our UK and Global Economic Outlooks from the people who wrote them:

Related News

news

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

Related Publications

Related events

Summer 2023 Economic Forum

11:00 to 12:00

11 August, 2023

Spring 2023 Economic Forum

11:00 to 12:00

12 May, 2023

Winter 2023 Economic Forum

11:00 to 12:00

10 February, 2023

Autumn 2022 Economic Forum

11:30 to 12:30

18 November, 2022

Summer 2022 Economic Forum

11:00 to 12:00

5 August, 2022

Spring 2022 Economic Forum

11:00 to 12:00

13 May, 2022

Winter 2022 Economic Forum

11:00 to 12:00

11 February, 2022

Autumn 2021 Economic Forum

11:00 to 12:00

12 November, 2021