Brexit and Covid put Winter Economy in Deep Freeze

Pub. Date

Pub. Date

Pub. Type

Pub. Type

Authors

Brexit and Covid put winter economy in deep freeze

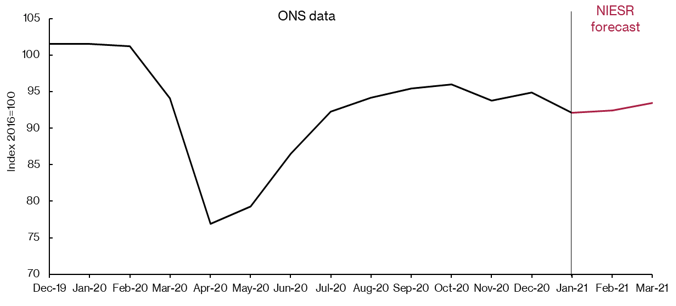

Figure 1 - UK GDP

Main points

- January’s smaller than expected fall in GDP means that we now estimate a contraction of 2.4 per cent in the first quarter of 2021. This would leave GDP in the first quarter of 2021 around 9 per cent lower than its level in the last quarter of 2019, before the pandemic struck.

- Real-time data and NIESR analysis imply that GDP is likely to resume its growth in February and March, by 0.3% and 1.1% respectively, on the back of higher contribution from government services and improving consumer confidence as infection rates come down.

- As a result, the first quarter of 2021 is likely to see a smaller contraction than widely anticipated, increasing the upside risks to our latest 2021 forecast of 3.4 per cent. However, the pace of recovery from the second quarter will crucially depend on how the opposing effects of the vaccine roll-out and lifting lockdown affect the path of Covid-19, as well as how consumers and businesses react.

- January’s data indicate that – while lockdown has reduced activity in some sectors to the levels of summer 2020 – other parts of the economy seem to have adapted and remain relatively unaffected. The health sector, responsible for rolling out the vaccines, grew by 6 per cent in January.

- The contraction in manufacturing at the start of 2021 is likely to be partly attributable to the unwinding of December pre-Brexit stockpiling and partly to permanent reductions in UK trade.

Rory Macqueen, Principal Economist - Macroeconomic Modelling and Forecasting, said: “While January’s lockdown has unsurprisingly hit the hospitality, retail and education sectors, returning to levels of output last seen in summer 2020, many other sectors have not been affected to anything like the same extent as they were last year. With February and March likely to see activity at similar levels, this provides further support for the view that the fall in the first quarter of 2021 may be smaller than expected. The pace of recovery from the second quarter will depend on whether vaccines continue to roll out according to plan, whether further mutations or outbreaks bring about a resurgence in the virus, and how quickly public confidence returns.”

Please find the full analysis in the document attached

Related Blog Posts

Related Projects

Related News

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

The Key Steps to Ensuring Normal Service is Quickly Resumed in the Economy

13 Feb 2023

4 min read

Related Publications

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

Spring 2023 Economic Forum

Winter 2023 Economic Forum

Autumn 2022 Economic Forum

Summer 2022 Economic Forum

Spring 2022 Economic Forum

Winter 2022 Economic Forum