Underlying Inflation Moderated Due to Weak Demand and Uncertainty

Pub. Date

Pub. Date

Pub. Type

Pub. Type

Authors

Underlying inflation moderated due to weak demand and uncertainty

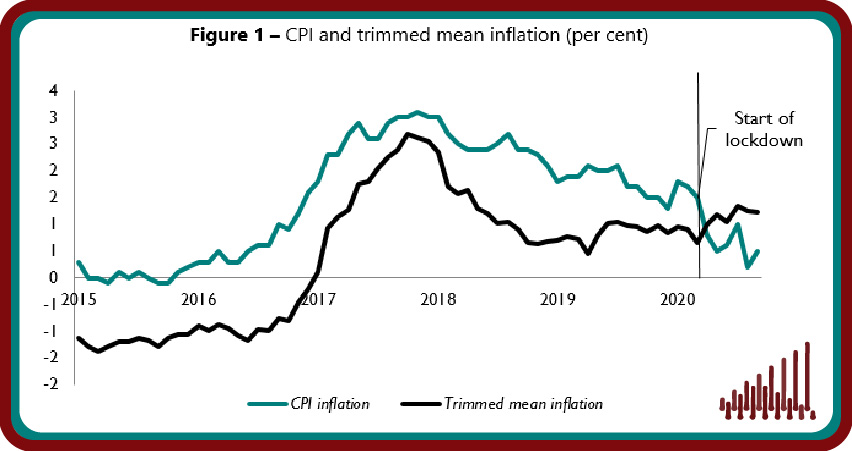

After moderating to a multi-year low of 0.2 per cent in the year to August 2020, headline inflation picked up incrementally to 0.5 per cent in the year to September 2020. Our new analysis of 118,876 locally collected goods and services indicates that prices remain muted across most categories except for the transport and restaurants and hotels. Increased mobility and a return to office-working following the lockdown likely contributed to increases in transport costs, while the unwinding of the government’s ‘Eat out to Help out’ scheme saw restaurants and hotels contribute 0.26 percentage points to the increase in headline inflation in September 2020.

Our measure of underlying inflation, which excludes the most extreme price changes, decreased to 1.2 per cent in September 2020, down from 1.3 per cent in August. Regional trimmed mean inflation reflects the diverging nature of the pandemic and local lockdowns: North West recorded underlying inflation of 0.7 per cent where cities like Liverpool, Manchester and Lancashire have faced higher Covid-19 uncertainty. The rapidly changing epidemiological environment and the implementation of the three-tier system is likely to weigh on already weak demand and employment prospects. Our analysis suggests that inflation for the rest of the year will stay subdued. Looking to the future, the headline CPI in the year to September 2021 is likely to undershoot the Bank of England’s inflation target of 2 per cent.

.PNG)

Main points

- Underlying inflation moderated to 1.2 per cent in the year to September 2020, as measured by the trimmed mean, which excludes 5 per cent of the highest and lowest price changes (figure 1).

- At the regional level, underlying inflation was highest in Wales at 2.4 per cent and lowest the North West and South West which saw an increase of only 0.7 per cent in the year to September 2020 possibly highlighting the different degrees of Covid-19 uncertainty across regions (table 1).

- 23.9 per cent of goods and services prices changed in September, implying an average duration of prices of 4.2 months, which is below the historical average of 5.2 months. 4.8 per cent of prices were reduced due to sales, 6.7 per cent fell for other reasons and 12.3 per cent were increases (figure 2).

- The historical relationship between current trimmed mean inflation and future CPI inflation implies CPI inflation is likely to stay below 2 per cent in the year to September 2021.

“Headline CPI inflation increased to 0.5 per cent in the year to September 2020, up from 0.2 per cent recorded in August, reflecting the higher transport costs and restaurant and hotel prices recorded during the month. Our measure of underlying inflation, which excludes extreme price movements, moderated to 1.2 per cent in September, and we assume that headline inflation will follow suit in the coming months. The imposition of further local lockdowns will weigh on already weak demand and employment prospects and are likely to keep inflation below 2 percent next year.”

Janine Boshoff

Economist, Macroeconomic Modelling and Forecasting

Related Blog Posts

Related Projects

Related News

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

Related Publications

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

Spring 2023 Economic Forum

Winter 2023 Economic Forum

Autumn 2022 Economic Forum

Summer 2022 Economic Forum

Spring 2022 Economic Forum

Winter 2022 Economic Forum