NIESR CPI tracker – September 2021 – Underlying inflation cautious against panic

Authors

.png)

Main points

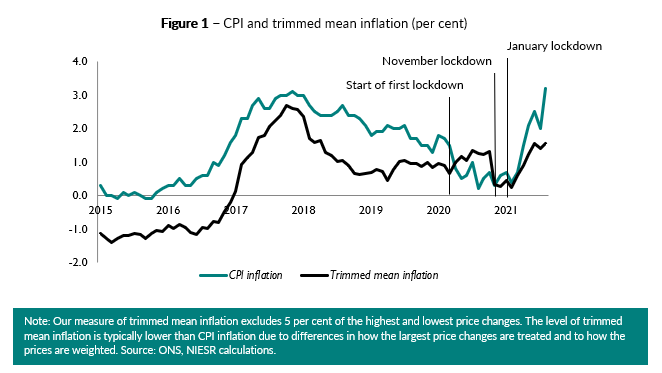

- While the headline consumer inflation increased by a large margin, from 2 per cent in July 2021 to 3.2 per cent in August, the rise in underlying inflation was more limited. Our measure of underlying inflation as measured by the trimmed mean, which excludes 5 per cent of the highest and lowest price changes increased to 1.6 per cent in August from 1.4 in July (figure 1), cautioning against panic regarding the surge in headline inflation number recorded in August 2021.

- As expected, base effects had a notable upward effect in August and will continue to add volatility to the annual headline inflation figure in the short term. NIESR calculations predicted the upward pressure in the August numbers, and we believe that September headline inflation will decrease due to base effects in September 2020.

- The most imminent transitory factor boosting consumer inflation numbers in the short-term is related to first scheduled reversal of the 2020 VAT cut in October 2021. Thereafter, the increase in OFGEM household energy price-cap scheduled for November 2021 will likely provide further impetus to consumer prices.

- 18 per cent of goods and services prices changed in August, implying an average duration of prices of 5.6 months. 3.7 per cent of prices were reduced due to sales, 4 per cent fell for other reasons and 10.4 per cent recorded increases (figure 2).

- Our measure of underlying inflation increased in most regions of the UK. Underlying inflation in London decreased to 2.7 per cent in August, down from 3.9 per cent in July. Scotland saw the lowest regional trimmed mean inflation of 1.1 per cent in August (table 1).

- Shortages in intermediate inputs and ongoing disruption in supply chains have filtered through to consumer goods prices, while labour shortages and the associated increase in wages could also feed through to headline inflation in the coming months.

- We expect headline inflation to remain elevated in the year to August 2022 and the Bank of England must now provide clear guidance on the inflation outlook and the likely path of policy rates and asset purchases to prevent a possible dislodging of inflation expectations.

“Annual headline inflation increased to 3.2 per cent in August from 2 per cent in July. Our measure of underlying inflation, which excludes extreme price movements, increased to 1.6 per cent in August from 1.4 per cent in July. The most recent volatility in the headline numbers reflects base effects: a moderation in July headline figures, followed by a stronger rebound in August, and we expect another decrease in annual consumer inflation in September. But as well as the base effect, the relatively high monthly rate of increase of 0.7 per cent contributed to the 1.2 percentage points rise in annual headline inflation in August reflecting cost pressures and the effects of reopening. There are important transitory factors that will boost headline inflation in the next few months. The imminent reversal of the 2020 VAT cuts, with the first hike scheduled in October 2021, as well as the scheduled increase in the OFGEM household energy price-cap in November 2021 will have the most pertinent effects in the short-term. We believe annual consumer price inflation will remain elevated in 2021 before peaking around 4 per cent in the first quarter of 2022. Since headline inflation is to remain above the Bank of England’s 2 per cent target in the short-term, the Bank’s future communications around tapering and policy rate normalisation will be crucial in preventing a possible dislodging of inflation expectations.”

Janine Boshoff

Economist, Macroeconomic Modelling and Forecasting

Please find full analysis by downloading the PDF document

Related Blog Posts

Related Projects

Related News

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

Related Publications

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

Spring 2023 Economic Forum

Winter 2023 Economic Forum

Autumn 2022 Economic Forum

Summer 2022 Economic Forum

Spring 2022 Economic Forum

Winter 2022 Economic Forum