Prospects for the UK economy: Forecast Summary

Pub. Date

Pub. Date

25 April, 2019

Pub. Type

Pub. Type

Authors

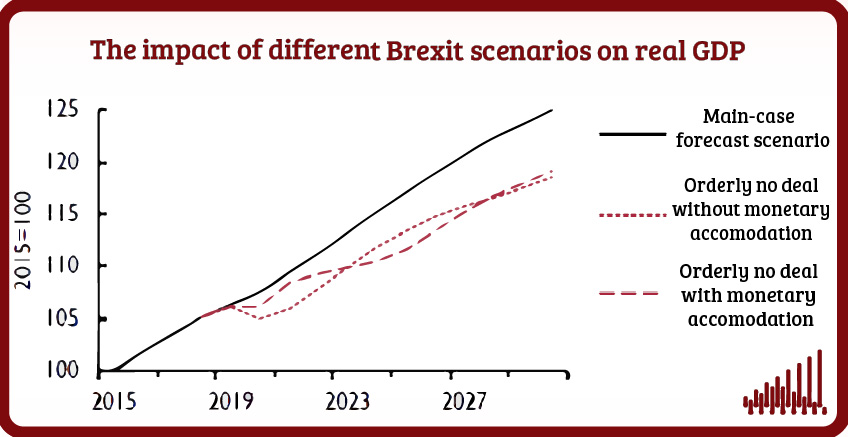

- The UK’s future relationship with the European Union (EU) remains undecided. Brexit-related uncertainty has led to investment plans being deferred and increased stockbuilding.

- Under our main-case forecast, based on a ‘soft’ Brexit and continuing uncertainty, GDP growth continues at around 1½ per cent in 2019 and 2020, broadly in line with potential output growth, and the unemployment rate stays at around 4 per cent.

- CPI inflation is forecast to remain around 2 per cent per annum as faster unit labour cost growth is offset by slower import price inflation. With inflation stable at target, and only limited evidence of domestic inflationary pressure, Bank Rate remains at 0.75 per cent throughout this year before being raised to 1 per cent in the second half of 2020.

- We expect public spending to rise more quickly than currently planned. That, together with the forthcoming reclassification of student loans in the public finances, is likely to mean that the government’s medium-term fiscal objectives will not be met.

- The current account deficit is forecast to fall from 4.2 per cent of GDP in 2019 to around 3 per cent in 2020, as domestic saving picks up relative to investment.

Read the press release here and the full forecast here

This open access is available as part of our ESRC IAA

.png)

Related Blog Posts

Related Projects

Related News

news

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

Related Publications

publication

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

11:00 to 12:00

11 August, 2023

Spring 2023 Economic Forum

11:00 to 12:00

12 May, 2023

Winter 2023 Economic Forum

11:00 to 12:00

10 February, 2023

Autumn 2022 Economic Forum

11:30 to 12:30

18 November, 2022

Summer 2022 Economic Forum

11:00 to 12:00

5 August, 2022

Spring 2022 Economic Forum

11:00 to 12:00

13 May, 2022

Winter 2022 Economic Forum

11:00 to 12:00

11 February, 2022

Autumn 2021 Economic Forum

11:00 to 12:00

12 November, 2021