Structural Change Needed to Escape Low-Growth Trend

Pub. Date

Pub. Date

Pub. Type

Pub. Type

Authors

Main points

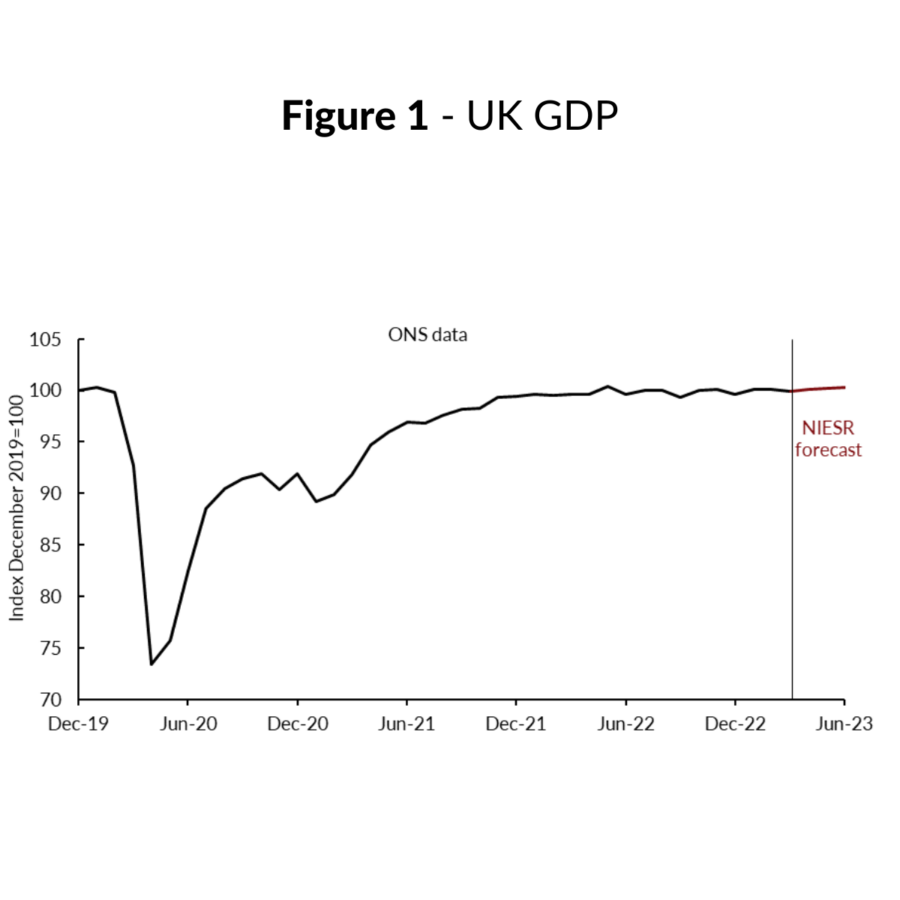

- Monthly GDP fell by 0.3 per cent in March 2023, following flat growth in February. This monthly figure was driven by a fall in services which offset monthly growth in construction and production.

- GDP grew by 0.1 per cent in the first quarter of 2023 relative to the previous three months, in line with our last most recent forecast. As shown in figure 1 below, the UK economy has largely flatlined following the initial stages of post-pandemic recovery; today’s monthly GDP is estimated to be only 0.1 per cent above its pre-pandemic (February 2020) level. As we stress in our latest UK Economic Outlook, for UK economic performance to ‘jump-start’ into a new era of high output growth, structural change will be needed.

- We expect that monthly GDP will bounce back in April, growing by 0.3 per cent relative to March, driven by growth in services. Indeed, the S&P Global/CIPS UK Services PMI reported an optimistic balance of 55.9 in April, up from 52.9 in March. Surveyed businesses noted a sustained rise in consumer spending in April, especially in the travel, tourism and leisure sub-sectors. However, a combination of high demand and still-high input costs meant that businesses continued to report passing on higher costs to clients, leading to an acceleration in the rate of price increase – this is concerning given the increasing embeddedness of inflation in the economy.

“Today’s data suggest that GDP grew by 0.1 per cent in the first quarter of 2023 compared to the fourth quarter of 2022, in line with our forecast published in last month’s tracker. Encouragingly, the services, production, and construction sectors all saw quarter-on-quarter growth – a further sign that the economy as a whole is exhibiting more resilience than previously thought. Though monthly GDP fell by 0.3 per cent in March following no growth in February, high-frequency data suggest that monthly GDP will bounce back strongly in April, likely driven by strong services performance. It is worth bearing in mind, however, that monthly GDP remains only 0.1 per cent above its February 2020 level – what we are seeing at the start of this year is (welcome) low growth, rather than a much-needed ‘jump-start’.”

Paula Bejarano Carbo, Associate Economist, NIESR

For a comprehensive summary and forecast of the UK economy, please see our latest UK Economic Outlook, published today.

Related Blog Posts

Related Projects

Related News

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

The Key Steps to Ensuring Normal Service is Quickly Resumed in the Economy

13 Feb 2023

4 min read

Related Publications

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

Spring 2023 Economic Forum

Winter 2023 Economic Forum

Autumn 2022 Economic Forum

Summer 2022 Economic Forum

Spring 2022 Economic Forum

Winter 2022 Economic Forum