UK Short-Term Interest Rate Expectations Retreat from Highest Level Since January 2020

Pub. Date

Pub. Date

13 December, 2021

Pub. Type

Pub. Type

Authors

Main Points

- We decompose long-term treasury yields into two components: expectations of the future path of short-term bond yields and a term premium. The term (or risk) premium is the compensation investors require for bearing the risk that short-term bond yields will not evolve as expected.

- The 10-year treasury yields peaked at 1.2 per cent on 21 October, the highest level since the start of the pandemic. This has been mainly driven by an increase in short-term interest rate expectations (figure 1). After the Bank contradicted market expectations by not hiking in November, the 10-year bond rate decreased to 0.8 per cent in December, largely on the back of a reduced term premium, remaining above the levels observed earlier in the year. The short-term interest rate expectations price-in the Bank rate going back to around its pre-pandemic 0.75 per cent level, and the reduction in the term premium suggests the market sees only a modest risk of it going higher than that.

- The adjustment in the UK risk premium is consistent with our latest GDP growth forecast: economic activity has continued to grow during the third quarter of this year but slower than expected, and is projected to increase by 1 per cent in the last quarter of 2021. The risk premium decreased from 0.54 per cent at the end of September to 0.15 per cent in December. Interest rate expectations, capturing markets’ expectations of rates over the longer horizon, increased to 0.94 per cent in October, the highest raise since the start of the pandemic, but have subsequently declined to around 0.65 per cent.

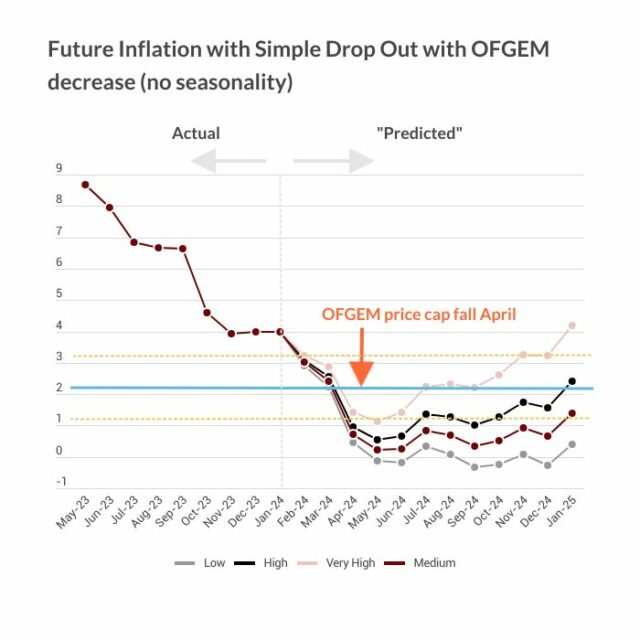

- The UK headline inflation having increased significantly to 4.2 per cent in October 2021 and now expected to peak at around 5 per cent in the second quarter of 2022. If inflation data continue to be strong, treasury rates may continue to rise, mainly driven by short term rate expectations.

- Many asset owners, e.g., of stocks and housing, and borrowers have benefited from central banks’ ultra-loose monetary policies. The increase in bond yields in October could be interpreted as a sign of impending problems, especially since a hike in policy rates will undoubtedly raise financial stability concerns.

- US government bond rates did not increase as much as in the UK, driven by a still negative term premium at the 10-year maturity, consistent with the estimates by the Federal Reserve Bank of New York. Interest rate expectations have increased to average 2 per cent since mid-November as the FOMC has signalled tightening policy sooner than expected given persistent upward inflation surprises.

- German 10-year Bund yields remains negative at -0.33, per cent. Euro area interest rate expectations turned marginally positive in October, but are now back in negative territory, partly reflecting concerns about the delta variant’s spread in Europe. The odds of the ECB increasing interest rates are thinner than in the UK and the US at the moment, as inflation overshooting the ECB target might be seen as a short interlude.

“Bond yields are higher than three months ago but have come off their peak. The level of UK inflation has convinced the market that rate hikes are coming, and so that short-run rate expectations have pushed bond yields higher in October. However, the Bank of England has delayed the first rate hike, which has calmed market fears about how rates might go and so the term premium has now declined."

Dr Corrado Macchiarelli

Research Manager for Global Macroeconomics

Related Blog Posts

Related Projects

Related News

news

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

news

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

news

The Key Steps to Ensuring Normal Service is Quickly Resumed in the Economy

13 Feb 2023

4 min read

Related Publications

publication

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

publication

UK Economy on the Road to Recovery in 2024 Following the Mild Recession

13 Mar 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

11:00 to 12:00

11 August, 2023

Spring 2023 Economic Forum

11:00 to 12:00

12 May, 2023

Winter 2023 Economic Forum

11:00 to 12:00

10 February, 2023

Autumn 2022 Economic Forum

11:30 to 12:30

18 November, 2022

Summer 2022 Economic Forum

11:00 to 12:00

5 August, 2022

Spring 2022 Economic Forum

11:00 to 12:00

13 May, 2022

Winter 2022 Economic Forum

11:00 to 12:00

11 February, 2022

Autumn 2021 Economic Forum

11:00 to 12:00

12 November, 2021