Walking the Line

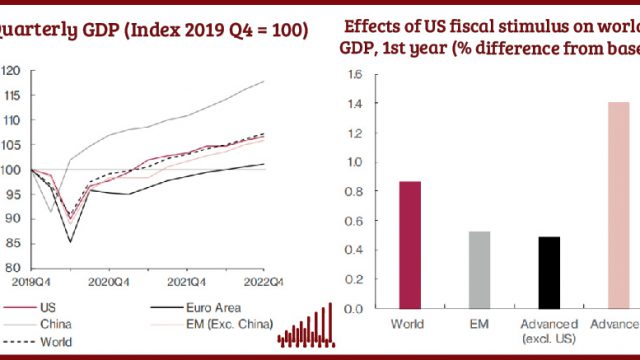

Our new world economy forecast, using NIESR’s global macro-econometric model, NiGEM, estimates that the effect of the war in Ukraine will result in the level of global GDP being over 1 per cent lower at the end of 2022 (about $1.5 trillion).

Sign in to Access Pub. Date

Pub. Date

11 May, 2022

Pub. Type

Pub. Type

Authors

External Authors

Summary

- Relative to our latest forecast in winter 2022, we are seeing the effects of supply side shocks stemming from the Russian invasion of Ukraine and the resulting international sanctions against Russia, and the scarring effect of Covid-19. Given this context, we are predicting lower GDP growth and higher inflation globally than previously envisaged.

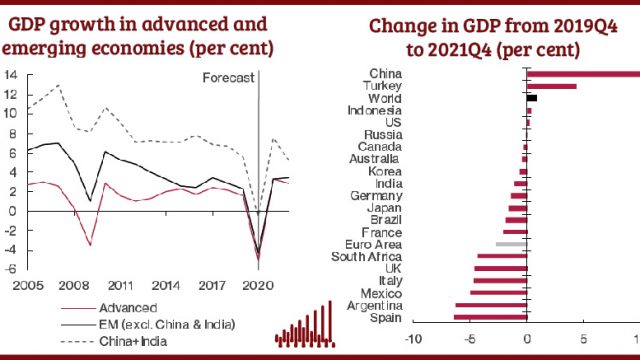

- The war in Ukraine and the resultant rapid increases in the prices of oil, gas, wheat and other commodities have substantially changed the near-term economic outlook, raising inflation, and heightening uncertainty and downside risks to economic activity. We have revised down our forecast for global GDP growth this year and next to 3.3 per cent and 3.2 per cent, from 4.2 per cent and 3.5 per cent, respectively. War-related recessions in Russia and Ukraine directly account for about half of that markdown.

- The new inflationary shock from the war threatens even higher inflation and we have increased our OECD inflation forecast for 2022 from 5.2 per cent to 8.2 per cent. So far, this year inflation has over-shot our expectations in the advanced economies and is expected to remain high as price pressures have broadened beyond volatile items such as energy and food, and these items have just suffered another upward shock.

- We continue to forecast that OECD inflation will slow in 2023 and 2024 but remain above 3 per cent. The very steep rise in commodity prices is assumed to level off and current evidence suggests that medium-term inflation expectations remain well-anchored and higher policy interest rates will bite into demand growth. But we forecast that inflation will remain elevated, averaging 4.4 per cent in 2023.

- We see considerable uncertainty around these projections given the changes to both economic and geo-political circumstances so far this year. A further escalation of international tensions, or the possibility that the effect of the observed higher fuel and food price rises might have a larger impact on emerging markets are among the key downside risks to our forecast.

- Higher than anticipated inflation has led to monetary policy tightening which will also contribute to slower GDP growth than previously forecast. We now expect the US Fed to raise policy interest rates to 2.25 per cent by the end of this year and 3 per cent by the end of 2023.

- Looking further forward, central banks will have to ‘walk the line’ between tightening policy enough to bring inflation down but not so much as to cause a contraction in activity.

Related News

news

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

news

1.2 million UK Households Insolvent This Year as a Direct Result of Higher Mortgage Repayments

22 Jun 2023

2 min read

news

The Key Steps to Ensuring Normal Service is Quickly Resumed in the Economy

13 Feb 2023

4 min read

Related Publications

Related events

Summer 2023 Economic Forum

11:00 to 12:00

11 August, 2023

Spring 2023 Economic Forum

11:00 to 12:00

12 May, 2023

Winter 2023 Economic Forum

11:00 to 12:00

10 February, 2023

Autumn 2022 Economic Forum

11:30 to 12:30

18 November, 2022

Summer 2022 Economic Forum

11:00 to 12:00

5 August, 2022

Spring 2022 Economic Forum

11:00 to 12:00

13 May, 2022

Winter 2022 Economic Forum

11:00 to 12:00

11 February, 2022

Autumn 2021 Economic Forum

11:00 to 12:00

12 November, 2021