NIESR Wage Tracker – July 2019

Pub. Date

Pub. Date

Pub. Type

Pub. Type

Authors

Pay growth at 11-year high but further acceleration unlikely

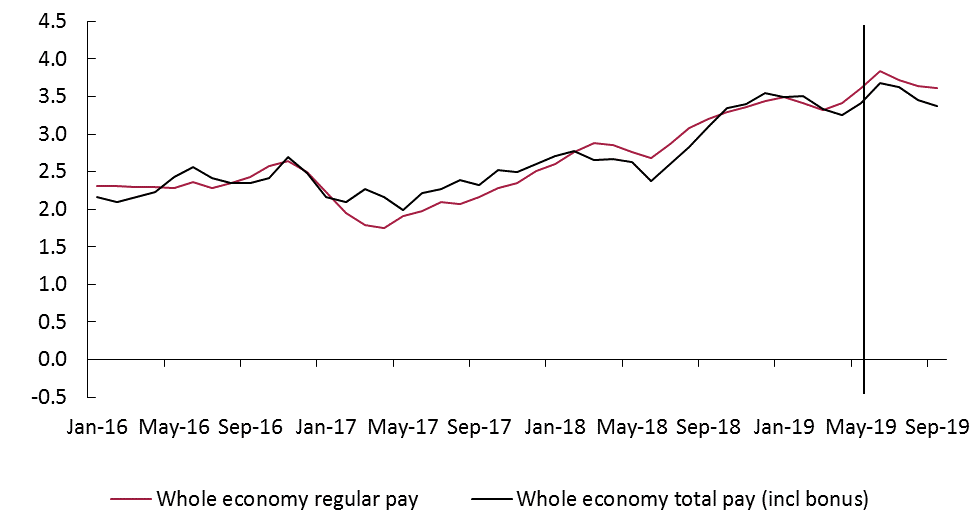

Figure 1: Average Weekly Earnings (3 months average year on year growth, per cent)

Source: NIESR, ONS.

Main points

- According to new ONS statistics published this morning, UK average weekly earnings (AWE) expanded by 3.6 per cent excluding bonuses (3.4 per cent including bonuses) in the three months to May compared to the year before (figure 1).

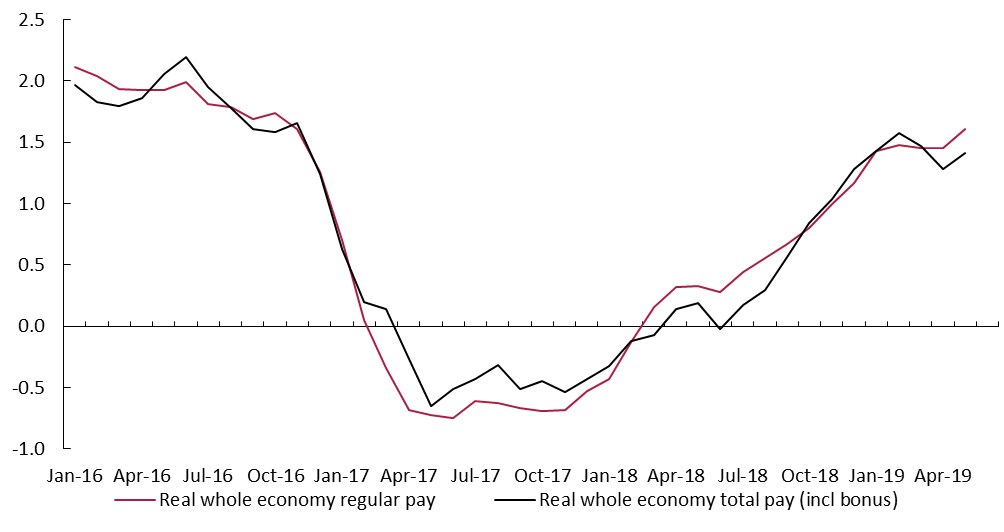

- With CPI inflation at 2 per cent in the three months to May, real wages excluding bonuses grew at an annual rate of 1.6 per cent over the same period, the strongest rate of regular real earnings growth since November 2016 (figure 2).

- Our Wage Tracker published last month had suggested that wage growth would continue to pick up modestly in May. This is confirmed by May data outturns which came in slightly stronger than predicted, partly as a result of upward revisions to April data.

- Going forward, the Wage Tracker indicates that regular pay growth will have reached 3.8 per cent in the second quarter of this year. Our first estimate for the third quarter of this year has regular pay growth stabilising at around 3½ per cent, reflecting survey evidence of a reduction in hiring and fewer vacancies.

- Based on NIESR Wage Tracker and GDP Tracker information, we estimate unit labour cost growth of around 3 per cent in the second and third quarter of 2019, up from just above 2 per cent in the first quarter.

Arno Hantzsche, senior economist at NIESR, said “Strong earnings growth in the first half of 2019 helped real pay recover most of the losses incurred since the financial crisis a decade ago. However, economic and political uncertainty pose a considerable risk to hiring activity and, according to our new estimates, prevent a further acceleration of earnings growth in the months ahead.”

Figure 2: Real whole economy AWE (3 months average year on year growth, per cent)

Source: ONS, NIESR.

Notes: Real pay growth is nominal pay growth deflated by a 3-month moving average of the consumer price index (CPI).

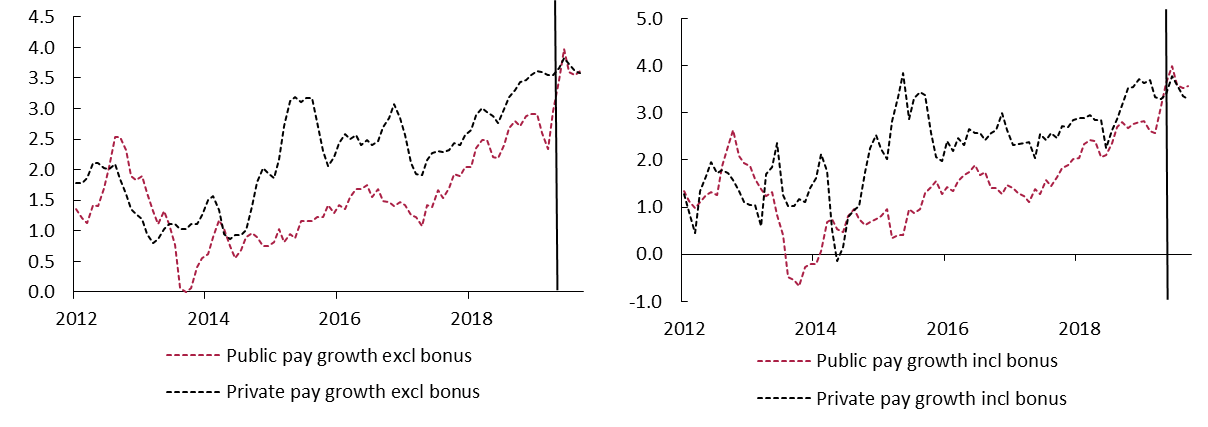

Figure 3: Public and Private sector AWE (3 months average year on year growth, per cent)

Source: ONS, NIESR.

Please find the full commentary in attachment

Related Blog Posts

What Are the Implications of the Rising National Minimum Wage and National Living Wage Rates?

19 Mar 2024

5 min read

Related Projects

Related News

Press Release: Compositional effects push up average weekly earnings at the end of 2020

26 Jan 2021

2 min read

Press Release: 2020 shaping up to be the worst year for total pay growth since 2009

15 Dec 2020

2 min read

Related Publications

Pay-Setting Among Employers in the Agriculture, Cleaning, Hospitality and Retail Sectors

11 Mar 2024

Research Report

Related events