Inflation Falls in November to 10.7%, but Monthly Inflation Remains Strong

In line with our forecast, CPI fell to 10.7 per cent in November from 11.1 per cent in October. The new month on month inflation was 0.4 per cent, which was outweighed by the big drop out from Nov 2021.

Authors

Month on month inflation remains well above the historic norms, and if sustained for a year would result in CPI inflation of 5 per cent, in line with our forecast in the “very high” scenario. Month on month inflation was positive for all types of expenditure except for communication, indicating that inflation is widespread. The five main contributors to the change in annual inflation in October were:

- Transport: -0.23 percentage points

- Alcohol and Tobacco: -0.08 percentage points

- Clothing and Footwear: -0.08 percentage points

- Recreation and Culture: -0.07 percentage points

- Restaurants and Hotels: 0.06 percentage points

The negative contributions were due to base effects of inflation dropping out from November 2021.

Month on month inflation was high for August 2021 to May 2022 (with the exception of January). So, as we move forward into 2023, to sustain or increase the headline inflation level, new inflation will need to come forward to replace what drops out from 2021/2. If the new inflation in 2022/3 is higher than the old inflation dropping out from 2021/2, we will see an increase in inflation; if the new inflation is lower, we will see a decrease. The inflationary story for the remainder of 2022 and into 2023 will be a tug of war between past inflation pulling down with the new inflation pulling up. In November 2022, we have seen the effect of past inflation dropping out dominating, dragging the inflation rate down.

The most important development in the last month was the implementation of the new EPG. The price of Electricity and Gas will be fixed from October 2022 to March 2023. The EPG will reduce CPI inflation in 2023 by about 2 percentage points from what it might have been without it.

The future path of inflation will also depend on how the Russo-Ukrainian war affects the world economy and the impact of sanctions imposed on Russia by the Western powers. On December 5th, the G7 and EU introduced a price-cap of $60 per barrel on exports of Russian oil. The main mechanism to enforce this is via the provision of insurance and other services by companies in the G7 and EU (details of the UK implementation are detailed in Russian oil services ban). It is too soon to see how well this price-cap is working and if the main customers of Russia (India and China) will go along with the price-cap or if the Russians can find alternative providers of insurance and related services required for oil shipment. The idea is that when the price-cap is operating, the G7 and EU countries can insure and provide services to expedite the supply of Russian oil and hence avoid a reduction in the world oil supply. However, the EU and UK have also banned the import of Russian oil and petroleum products, which may cause the supply of oil to the UK and EU to fall and its price increase.

The supply of natural gas is highly inelastic in the short run as is the demand. Reductions in Russian supply have led to a dramatic rise in price and an increase in expenditure and hence the revenue of gas suppliers. Whilst the EPG will reduce CPI inflation in the UK, it will not increase the supply of natural gas, or the real price (net of the subsidy) paid to gas suppliers. This will mean that the EPG makes energy shortages and power cuts more likely as the subsidy will mean that demand will remain high and with the same supply this may imply rationing by power cuts (depending on the weather in the coming months). In the longer run (3-5 years) it will be possible to replace most Russian gas across the EU, for example with a new pipeline for Israeli gas and with more expensive LNG from a variety of sources. In the shorter run, some European governments, including Germany, are reversing the phasing out of coal-fired and nuclear power stations to try to fill the short-run gap.

However, a positive effect of the increase in the fossil fuel price is that it will speed up the transition to renewable and other alternatives. Also, the slow-down in economic activity it causes serves naturally to reduce the emissions of carbon. More widely, a slowdown in growth in the World as the cost-of-living crisis affects real incomes and leads to a reduction in discretionary consumer expenditure may lead to a decline in some commodity and energy prices across the world. This may mitigate the inflationary pressures somewhat, as we have already seen with petrol prices in the UK.

China’s zero Covid policy has had a major impact on the Chinese economy and global supply chains in 2022. The Chinese government has started to ease the zero Covid policy, in response to protests across the country against the lockdowns imposed as part of the policy. This is a positive development and should lead to a freeing up of world supply chains originating in or passing through China, which will have a downward effect on inflation.

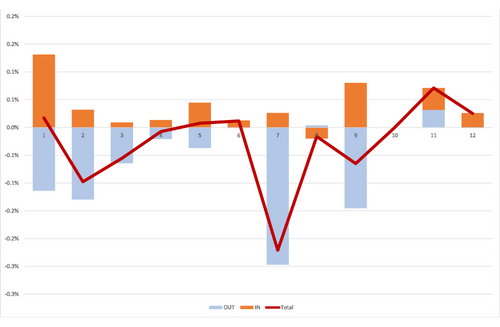

Turning back to the October inflation figures, we can look in more detail at the contributions of the different sectors to overall inflation in Figure 1, with the old inflation dropping out of the annual figure (October-November 2021) shown in blue and the new monthly inflation dropping in (October-November 2022) shown in Brown, using the expenditure weights to calculate CPI. The overall effect is the sum of the two and is shown as the burgundy line.

We can see that for most types of expenditure, there are significant drop-outs from the previous year (the Blue team) and drop-ins from the current year (the Brown team). The change in inflation is the result of the tug-of-war between the Blue and Brown teams, and this will continue for the rest of 2022 and into 2023. November is a clear win for the Blue team, with big drop outs in several sectors, especially Transport. However, we can also see that in most sectors there is new inflation coming in.

Figure 1: CPI November 2022: Contributions by type of expenditure (in and out)

Sectors: (1) Food and non-alcoholic beverages; (2) Alcoholic beverages and tobacco; (3) Clothing and footwear; (4) Housing, water, electricity, gas and other fuels; (5) Furniture, household equipment and maintenance; (6) Health; (7) Transport; (8) Communication; (9) Recreation and culture; (10) Education; (11) Restaurants and hotels; (12) Miscellaneous goods and services

Extreme Items

Out of over 700 types of goods and services sampled by the ONS, there is a great diversity in how their prices behave. Each month some go up, and some go down. Looking at the extremes, for this month, the top ten items with the highest monthly inflation are:

| Table 1: Top ten items for month-on-month inflation (%), October 2022 | |

| CD ALBUM (NOT CHART) | 34.88 |

| SMART SPEAKER | 21.08 |

| FRUIT DRINK BOTTLE 4-8 PACK | 18.07 |

| COMPUTER GAME 2 | 17.62 |

| MUSIC DOWNLOADS | 16.31 |

| PREMIUM POTATO CRISPS/CHIPS | 14.47 |

| PRE-RECORDED DVD (NON-FILM) | 12.26 |

| INTERNET COMPUTER GAMES | 11.15 |

| TABLET COMPUTERS | 10.83 |

| GIRLS JACKET (5-13 YEARS) | 10.78 |

Not a good month for music lovers. The ten items with the highest negative inflation this month are shown in Table 2.

| Table 2: Bottom ten items for mom inflation (%), October 2022 | |

| SELF TANNING PRODUCT | -6.88 |

| HOTEL 1 NIGHT PRICE | -7.11 |

| CREAM LIQUER 70CL-1LT 14-20% | -7.81 |

| BOOK – FICTION – HARD COVER | -8.18 |

| ELECTRIC HEATER -SEASONAL | -8.27 |

| WOMEN’S JEANS- BRANDED | -8.35 |

| CHILD’S TRAINERS-SPORTS | -8.44 |

| EURO TUNNEL FARES | -8.74 |

| AIR FARES | -10.12 |

| MOBILE PHONE APPLICATIONS | -34.35 |

November was a good month for a getaway, whether a staycation in a hotel, or travel abroad.

In both these tables we look at how much the item price-index for this month has increased since the previous month, expressed as a percentage. These calculations were made by my PhD student at Cardiff University, Yang Li.

Looking Ahead: Ukraine and Beyond

We can look ahead over the next 12 months to see how inflation might evolve as the recent inflation “drops out” as we move forward month by month. Each month, the new inflation enters the annual figure and the old inflation from the same month in the previous year “drops out”. However, the invasion of Ukraine by Russia and the western sanctions in response continue to make things uncertain. That said, the invasion and sanctions are certainly going to continue to sustain inflation as we go forward. We have therefore adjusted our four scenarios:

- The “medium” scenario assumes that the new inflation each month is equivalent to what would give us 2 per cent per annum – 0.17 per cent per calendar month (pcm) – which is both the Bank of England’s target and the long-run average for the last 25 years. This is a reference point only, as inflation will be well above this level for the next year.

- The “high” scenario assumes that the new inflation each month is equivalent to 3 per cent per annum (0.25 per cent pcm).

- The “very high” scenario (our central forecast) assumes that the new inflation each month is equivalent to 5 per cent per annum (0.4 per cent pcm). This reflects the inflationary experience of the UK in 1988-1992 (when mean inflation was 0.45 per cent). It also reflects the continuation of the UK average in the second half of 2021. This level of month-on-month inflation would indicate a significant break from the historic behaviour of inflation from 1993-2020.

- The “Sanctions” scenario. This assumes that new inflation per month is 0.8 per cent, equivalent to 10 per cent per annum. This is a high figure, which is unlikely to be sustained for a prolonged period unless geopolitical conditions deteriorate.

We have added the “Sanctions” scenario since March 2022 to reflect what we can expect as sanctions and the war itself affect global energy and commodity prices. We have dropped the “low” scenario from previous releases as this is now irrelevant. The “Very high” scenario is the central forecast, but of course there is very high uncertainty now. Month on month inflation has averaged over 1 per cent since February 2022, but the new inflation in November 2022 was in line with the very high scenario (and hence the forecast was correct).

We expect inflation to peak in January 2023. The exact level of inflation at the peak remains uncertain, and will depend very much on the intensity of January sales and may well be less than the 11.1 per cent predicted by the very high scenario. Our forecast is for a slight fall in inflation in December, to 10.6 per cent.

In all scenarios, there is a rapid fall in inflation from February 2023, which is due to the drop out of the high inflation figures in the corresponding months this year. However, inflation will remain well above 3 per cent for the whole of 2023 and NIESR’s current forecast is that it will not return to target until mid-2025. There will be a significant change in expenditure weights used to calculate inflation, with energy related expenditures being given more prominence in the “consumer basket” in 2023. If energy prices subside quickly, this might lead to a more rapid fall in the headline CPI inflation rate.

This forecast assumes that geopolitical tensions do not deteriorate. An escalation of the war in Ukraine and direct conflict between Russia and NATO would rapidly worsen the picture for inflation. Looking east, if the rising tensions between the US and China lead to an intensification of the trade war or even open military conflict in the South China sea or Taiwan (Republic of China), world supply chains would be disrupted, and inflation significantly raised. However, the recent local elections in Taiwan, with good results for the opposition KMT party which supports the “one China” policy and opposes the separatist government suggests that the Taiwan issue may calm down for some time. There may be a negotiated settlement to end the war in Ukraine in 2023, which would stabilise the economic situation and lead to a reduction in commodity and energy prices, especially if sanctions are eased.

Figure 2: Looking forward to November 2023: Future inflation with simple drop-out with Ofgem increases (no seasonality)

Related Blog Posts

Related Projects

Related Publications

A Neural Network Approach to Forecasting Inflation

09 May 2024

UK Economic Outlook Box Analysis