The wage Phillips curve – another piece of the puzzle

A debate is raging among both academics and policymakers whether wage growth and unemployment still form a negative relationship, in other words, whether the wage Phillips curve is alive.

Authors

A debate is raging among both academics and policymakers whether wage growth and unemployment still form a negative relationship, in other words, whether the wage Phillips curve is alive. Roughly until the global financial crisis, periods of low unemployment meant the bargaining power of workers was high, leading to increases in pay. In recent years, exceptionally low levels of unemployment in a number of advanced economies have surprisingly not generated substantial wage pressure. The (wage) Phillips curve relationship between (wage) inflation and slack in the economy forms a core building block of conventional macroeconomic models. It also provides the theoretical basis for inflation-targeting monetary policy. A number of explanations have been brought forward for the recent flattening of the curve. Researchers at the IMF conclude that nominal wage growth remains subdued because inflation expectations are very much anchored to central banks’ targets. This, however, does not explain the widespread weakness in real wage growth.

Through a series of blogs NIESR has recently explored alternative solutions to the puzzle. Bell and Blanchflower argue that headline rates of unemployment conceal the fact that many of those in employment would actually prefer to work longer hours. Once this additional slack in the labour market is exhausted, wages should rise. Yet even in places where underemployment is low, like Germany, wage growth remains below pre-crisis levels. Kara and Lopresto find that low rates of (labour) productivity growth have been a major drag on real wage growth in recent years. What remains open then, is what held back productivity from rising more rapidly. The long shadow of the Great Recession, i.e. hysteresis, may also play a role in holding back wage growth (cf. Blanchard 2018) and Farmer and Nicolò (2018) argue that it is beliefs about the state of the economy that create this persistence. In this blog post, I argue that a structural change has taken place that has shifted the main adjustment mechanism of labour markets away from wages to employment.

In principle, an employer has three levers to alter the overall wage bill in response to changes in demand: the real wage per hour worked, the hours per worker that are reimbursed, and the number of workers employed. In a recently published paper my co-authors and I study the adjustment of labour markets along these three margins to shocks to financial conditions across sectors of euro area economies. We are particularly interested in the extent to which labour market institutions affect which adjustment margins are employed. Institutions like employment protection legislation and union density vary widely across countries and sectors but have recently been liberalised to improve the flexibility of economies. Mantra-like, the President of the European Central Bank and EU officials kept reminding governments to undertake structural reforms in order to buffer the currency union from future crises.

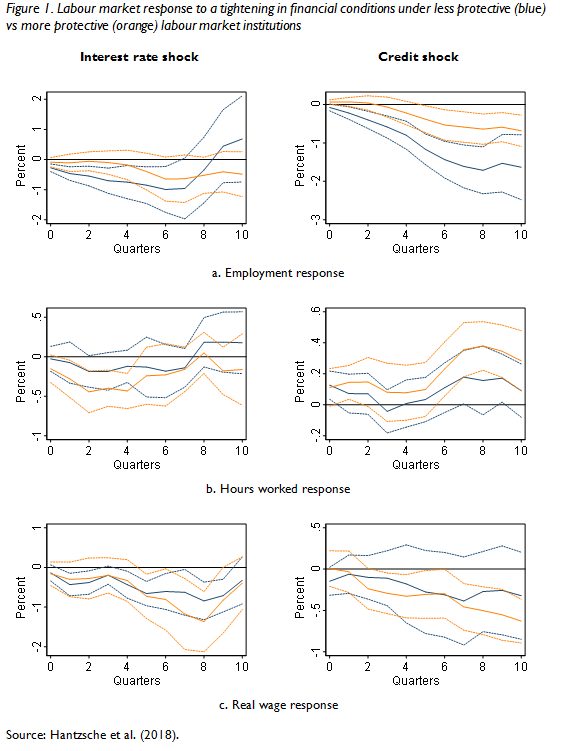

We find that in a labour market with low degrees of employment protection the adjustment is moved from wages, and to some extent hours worked, to employment, leaving the adjustment of the overall wage bill mainly unchanged. This is illustrated in Figure 1, which plots the response of the three adjustment margins to two types of (tightening) financial shocks, a shock to interest rates (left column) and a shock to the provision of credit (right). These shocks can be thought of as shocks to aggregate demand. While in more protected sectors (orange line), employment moves much less after the shock, less protected sectors (blue line) see a much stronger employment response. This is mirrored by a somewhat more pronounced response of real wages and hours worked in protected sectors relative to less protected sectors. We also find that employment recovers much more quickly in liberalised sectors as financing conditions ease, than in rigid sectors, where wages pick up more strongly.

Note: Less protective institutions blue line (20th percentile of sample employment protection legislation); more protective institutions orange line (80th percentile of sample employment protection legislation). Dashed lines 90% confidence interval calculated with Driscoll-Kraay standard errors. Responses are estimated using the local projections method separately for the three labour market variables and the two types of financial shocks. We control for the growth rate of gross value added, the composition of the employed labour force, country-sector-specific trends and time-fixed effects. The sample covers manufacturing, construction and services sectors of 15 euro area countries over 1999Q1 to 2015Q4.

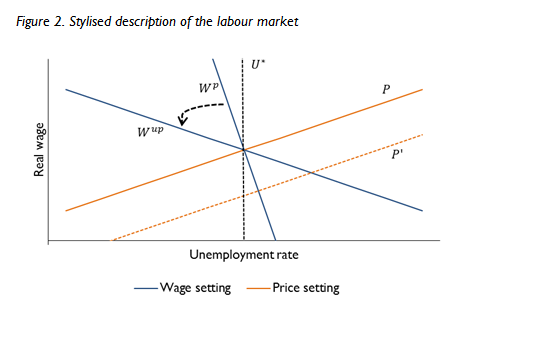

This suggests that recent labour market reforms, that made it easier to lay off workers during downturns, led firms to adjust their wage bill increasingly through employment and less through wages, holding wage growth down. To illustrate this, Figure 2 provides a stylised description of the labour market. As unemployment decreases, the marginal cost of production increases leading firms to charge higher prices (price setting P). This can be interpreted as a labour demand relationship. A standard labour supply relationship implies that wages are negatively related to unemployment (wage setting W): low unemployment makes it easier for workers to ask for a pay rise. The structure of the labour market determines how sensitive wages are to changes in unemployment. In protected sectors (Wp), employment can be thought of as relatively less flexible. A shock to aggregate demand (P’), mainly leads to an adjustment of wages. In less protected sectors (Wup), on the other hand, the same type of demand shock causes a much larger adjustment of employment (and therefore unemployment) relative to wages. This holds independent of the long-run level of unemployment consistent with stable inflation (NAIRU U*), which may also respond to changes in the bargaining power of workers.

Besides reforms of labour markets other structural changes are likely to have had similar effects on the adjustment mechanism of labour markets. Globalised trade, cross-border outsourcing and international migration mean that workers not only compete for jobs domestically but across the globe, weakening their bargaining power. The move in developed countries from manufacturing-based production to a service sector economy with high degrees of casual and part-time work may also keep wages low while requiring employment to be flexible.

The structural change in adjustment margins from wages to employment has likely contributed to high levels of employment in the aftermath of the crisis as well as low wage inflation. A flipside is low labour productivity, given that output growth has not much changed. An implication is that even if underemployment is being reduced, workers may first demand an adjustment of the type and quality of employment before asking for a wage increase. For instance, recent wage negotiations in Germany’s metal sector showed that labour unions are willing to trade pay rises for more worker-friendly employment contracts.

Could it therefore be that President Draghi’s call for more flexible labour markets, while helping to bring unemployment down, has made it more difficult for the ECB to meet its inflation target? More fundamentally, the structural change in labour markets may have caused a longer-term weakening of the wage Phillips curve by making wage setting less responsive to the business cycle.

Reference: Hantzsche, A., Savsek, S., & Weber, S. (2018). Labour market adjustments to financing conditions under sectoral rigidities in the euro area. Open Economies Review. – Disclaimer: The views expressed in this blog are my own and do not necessarily reflect the views of my co-authors and the institutions they are affiliated with.

Further suggested reading:

Related Blog Posts

What Are the Implications of the Rising National Minimum Wage and National Living Wage Rates?

19 Mar 2024

5 min read

Related Projects

Related News

Press Release: Compositional effects push up average weekly earnings at the end of 2020

26 Jan 2021

2 min read

Press Release: 2020 shaping up to be the worst year for total pay growth since 2009

15 Dec 2020

2 min read

Related Publications

Pay-Setting Among Employers in the Agriculture, Cleaning, Hospitality and Retail Sectors

11 Mar 2024

Research Report

Job Boom or Job Bust? The Effect of the Pandemic on Actual and Measured Job and Employment Growth

07 Feb 2024

UK Economic Outlook Box Analysis

Kurzarbeit/Short Time Working: Experiences and Lessons from the Covid-Induced Downturn

20 Nov 2023

National Institute Economic Review

Related events