Government Bond Term Premia During the Pandemic

Pub. Date

Pub. Date

Pub. Type

Pub. Type

Authors

This is a preview from the National Institute Economic Review, November 2020, no 254.

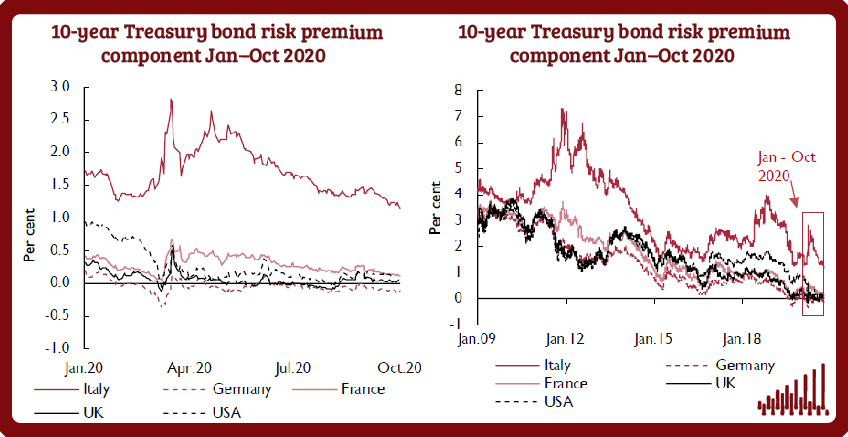

The Box examines the behaviour of government bond yields in the US, the UK and Europe, assessing – in particular – whether investors have demanded higher term premia following an upsurge in uncertainty since the Covid-19 shock. The evidence suggests that central banks’ asset purchase programmes such as quantitative easing, as well as higher savings and lower investment demand, resulted in term premia which do not compare in scale with what was observed at the height of the Global Financial Crisis.

The analysis in this Box has been prepared by NIESR Principal Economist Corrado Macchiarelli.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

The Financial (In)Stability Real Interest Rate, R**, as a Monetary Policy Constraint

07 Feb 2024

Global Economic Outlook Box Analysis

Geopolitical Risks and the Global Economy

07 Feb 2024

Global Economic Outlook Box Analysis

The Spectre of a US House Price Correction

07 Feb 2024

Global Economic Outlook Box Analysis

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum