The UK’s Brave New World

One reason for the UK leaving the EU was the promise of ‘taking back control’ of trade policy. The UK would give up its influence and vote on EU policies in return for the freedom to negotiate its own trade agreements with countries around the world.

Authors

One reason for the UK leaving the EU was the promise of ‘taking back control’ of trade policy. The UK would give up its influence and vote on EU policies in return for the freedom to negotiate its own trade agreements with countries around the world.

It is more than four decades since the UK last took the lead in trade negotiations. Back then, exports were mostly domestic manufactured goods where a pound of exports meant a pound of local profits and wages. Today, UK firms operate complex global supply chains where services generate more than half of its domestic profits and wages from trade. This matters when negotiating the best type of trade arrangements. Trade policy is no longer just about tariffs and subsidies, but common standards and regulation, investment protection and free movement of ideas and human capital.

Three sets of trade talks

First, the UK has to enter into a new governance arrangement with the EU. The now famous Article 50 of the Treaty covers the process of separation from the EU and includes reference to the future economic arrangements. But the precise terms of these arrangements will be part of a separate agreement, that must be unanimously agreed by the remaining 27 member states, and even ratification in some national assemblies. The complexity of this new governance arrangement suggests an interim arrangement may be required.

Second, on leaving the EU the UK must re-negotiate its WTO membership agreement. There is no precedent for this particular process, and the UK will need to agree its terms of engagement outside of the EU with the other 160 member states (establish ‘Most Favoured Nation’ terms). The most expedient approach may be to transpose, where appropriate, most of the existing commitments under its the EU membership to avoid a lengthy negotiation.

Third, the UK will no longer be covered by the EU’s 53 Preferential Trade Agreements (PTAs) (mostly with developing states). It may look to strike similar agreements along new or different lines. The UK would also need to consider if, and how, to be included in the Trans-Pacific Partnership which was agreed this year but yet to be ratified and other negotiations including the controversial US-EU Transatlantic Trade and Investment Partnership. Whether the UK has more success or less influence outside the EU remains to be seen.

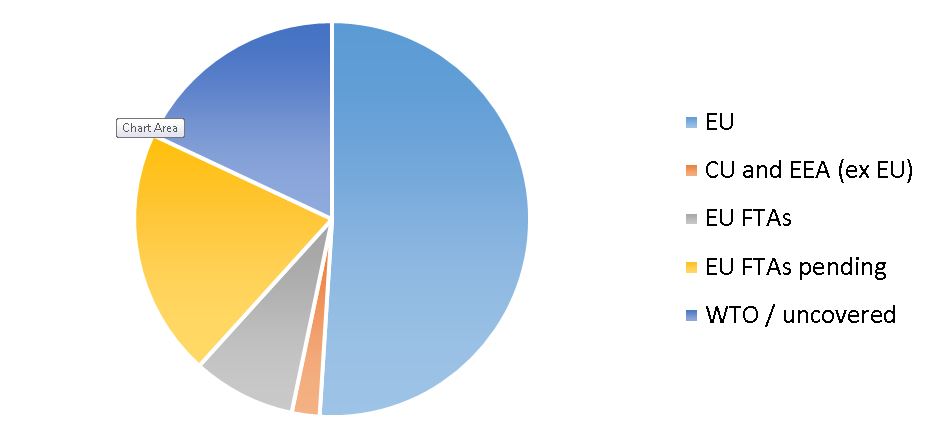

Figure 1 puts these tasks into perspective. Just over half of UK trade is with the EU. If we add the other countries in the European Economic Area (EEA) and Turkey in the customs union (CU), the share of trade is 53%. Including those countries that have existing PTAs with the EU covers 62% of UK trade. Finally, including countries which are currently negotiating PTAs with the EU covers 82% of total UK trade. Most of the remaining UK trade is covered by WTO agreements.[1]

Figure 1: Share of total UK trade covered by trade agreements

Source: ONS and EC DG Trade

EU priorities

The first priority is with the largest trade partner. One of the most pervasive results in trade studies is that distance matters: surveys suggest that doubling the distance between trading partners results in almost halve the amount of trade. Surprisingly, the rise in global supply chains makes distance more, rather than less, important. Proximity is especially important for intermediate trade: as production becomes more fragmented, distance appears to matter more.

The UK will have to first establish new trade arrangements with the EU as the basis for agreements with other countries. Each option involves a trade-off between access to the Single Market and control over economic policy leavers. As a member of the EEA (e.g. Norway) the UK would have access to the Single Market but without a vote on the regulations or access to the same courts to settle disputes. EEA involves accepting the free movement of labour, or at least with minimal temporary restrictions. UK exports would be subject to ‘rules of origin’ to tax the intermediate trade from outside of the EU.

The second option is for the UK to re-join the European Free Trade Association (EFTA). This is similar to the EEA option, but with less access to the Single Market. The only ETFA country that is not a member of the EEA is Switzerland which has full Single M access for goods trade but is required to strike bilateral treaties to secure access for specific services. This is a significant cost. Many services, for example financial services, are carried out through a third countries such as the UK. Switzerland makes a smaller per capita contribution to the EU budget than Norway in the EEA to reflect the lower level of market access.

Industry priorities

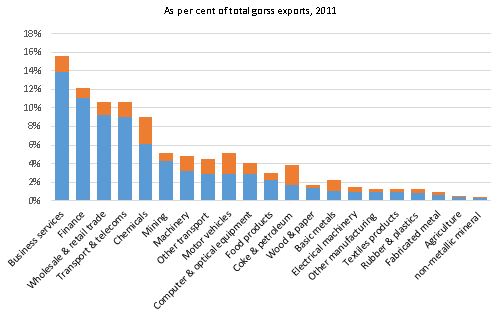

The UK must also consider the market structure of its most successful industries. It is important to know which sectors generate the most value added for UK firms. According to OECD statistics, UK service sector firms generated 52% of the value added (the latest data is for 2011) in total exports. A short animation shows why trading services is fundamentally different to trading goods. The right to establish firms in overseas markets, the same rules and regulations, mutual recognition of providers and free movement of labour are all necessary for being part of a Single Market for services exports.

Figure 2 gives a break-down of value added by domestic (blue) and foreign (orange) firms in UK exports by the most important trading sectors. It is striking that business services, finance and wholesale and retail trade account for the same domestic value added as the seventeen other sectors from chemicals onwards. For these businesses trade policy is about market access, equivalent regulations and mutual recognition. Many FTAs include service sector provisions, but they typically involve official procurement opportunities, cross border exports of services (as opposed to locating firms in foreign markets), transparency agreements and cover specific sectors only. No FTAs offers anything like the service sector access as the Single Market.

Figure 2: Domestic and Foreign Value Added in Exports by Industry

Source: OECD Trade in Value Added Tables, 2011 data

Conclusion

The challenge for trade negotiators is to get the best possible package for each of the alternative trade arrangements. But it is ultimately for politicians to decide how the preferences of UK citizens might best map onto these alternative arrangements. From an economics perspective, it is clear that agreements offering deep market access are more preferable than WTO access and many FTAs. The problem is that policies which enable deep market access encroach on the traditional domain of domestic policy. The optimal solution is to combine future trade arrangements with domestic policy. The Brave New World is finding out how to take the gains from trade while compensating for the social costs.

[1] All data are from the IMF Direction of Trade Statistics 2015.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum