Uncertainty shrouds the Italian elections but the economic tide is strong

Unlike the 2013 elections and the recent French elections, the outcome of the Italian elections due 4th March is hardly predictable, and that’s due to the fracture of the country into three main blocks, the centre-right coalition, the 5Star Movement, and the Centre-left coalition.

The most recent polls point to the centre-right coalition composed of Berlusconi’s backed Forza Italia, the League (previously known as the Northern League) and Brothers of Italy having roughly 37% of the support. With around 28%, the 5Star Movement currently stands as the biggest single party list. Finally, the centre-left coalition with an estimated 27% of the votes has seen a strong decline in support over the past years. The fragmentation of the country into three main blocks makes the formulation of the outcome highly challenging.

Authors

Unlike the 2013 elections and the recent French elections, the outcome of the Italian elections due 4th March is hardly predictable, and that’s due to the fracture of the country into three main blocks, the centre-right coalition, the 5Star Movement, and the Centre-left coalition.

The most recent polls point to the centre-right coalition composed of Berlusconi’s backed Forza Italia, the League (previously known as the Northern League) and Brothers of Italy having roughly 37% of the support. With around 28%, the 5Star Movement currently stands as the biggest single party list. Finally, the centre-left coalition with an estimated 27% of the votes has seen a strong decline in support over the past years. The fragmentation of the country into three main blocks makes the formulation of the outcome highly challenging.

The cycle is strong but the structural problems remain

Against a backdrop of potential scenarios, we believe that the outcome of the Italian elections should not disrupt the ongoing economic recovery at least in the near-term. However, the structural issues the economy faces, such as the high unemployment level, burdening fiscal position and abysmal productivity growth, are at risk faced with political instability and lack of reforms.

GDP growth gained momentum in the third quarter of 2017 to a rate of 1.7 per cent year-on-year, the strongest since 2011. The stronger performance of the economy seems to be broad-based, driven by solid domestic demand and the strength in global growth. Economic sentiment indicators in 2017 have painted a healthy picture of growth, and the manufacturing PMI reached a near seven-year high in January 2018.

Accordingly, we expect GDP growth to be steady over the near-term forecast period, at around 1.4 per cent in 2018 and 1.3 per cent in 2019. This is significantly above our estimate of potential output (figure 1). The currently accelerating GDP, rising economic sentiment, and decreasing financial vulnerability of families and banks should trump any political instability potentially that might arise from these elections.

.PNG)

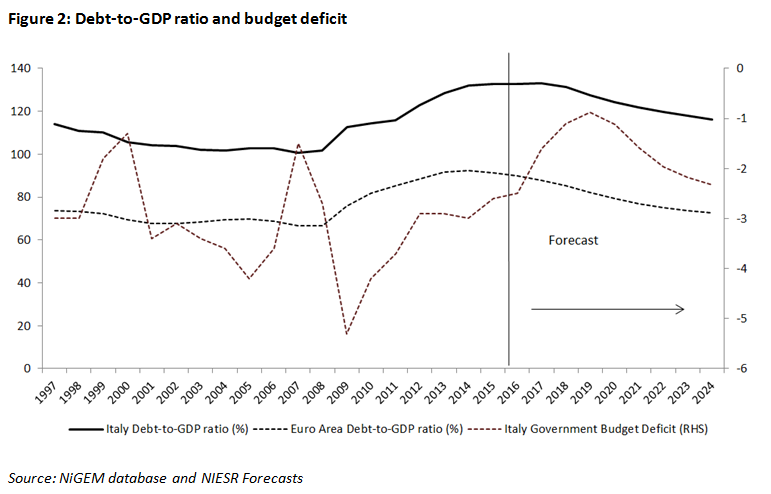

That said the positive economic cycle underway does not diminish the structural problems Italy faces. Unemployment at 12 per cent is still above pre-crisis levels and significantly higher than the Euro Area average. High youth unemployment will feed into higher structural unemployment as those long unemployed and unexperienced will face difficulties in re-entering the labour force. The public sector debt-to-GDP ratio remains significantly above the Euro Area average and therefore Italy must maintain a primary surplus to stabilise its large fiscal debt. The agenda of many political parties stress on fiscal stimulus measure, which might threaten the debt sustainability further.

The large stock of non-performing loans (NPLs) held by banks has been shrinking since mid-2017, tackled by the government rescue package of 1.2 per cent of GDP. This was aided by the strong cycle and pressure from the European Central Bank on banks to improve their balance sheets. Yet, bank lending remains hampered. All in all, Italy is past the acute stage of the crisis, but some ten years after the peak in 2007, the economy is still around 5 per cent smaller, and we expect GDP to recover to the pre-crisis level by 2020 only, which suggests that well over one decade worth of growth has been lost.

Most likely outcome of the elections

The most straight-forward outcome sees a centre-right coalition government. Italian polls have a quite significant margin of error, but the coalition is not too far from an outright majority. Also, looking at the historical series of the polls, while support for the ruling Democratic Party (the biggest party in the centre-left coalition) has been trending downwards since mid-2017, and for the 5SM has remained quite stable since around 2015, it has grown firmly for the main party of the centre-right coalition (Forza Italia).

.PNG)

If the centre-right wins, markets’ response will probably be positive, as the uncertainty dominating the Italian political scene would finally dissipate, and so would the fears of a takeover of the government by populist and Euro-sceptical parties. However, investors have not forgotten the crisis of Berlusconi’s government in November 2011, when the yield of the two-year government bond exceeded 9%, so a possible deepening of the spread between Btp-Bund is not unlikely. More importantly, the inconsistencies around the policy agenda across the parties of the coalition (Forza Italia, the League and Brothers of Italy) would create issues going forward, especially around how to deliver the proposed fiscal policy (the so-called “Flat tax” on personal and corporate income) and potential policy reversals, in particular with regards to the European integration.

Other scenarios

While a centre-right coalition government is the most likely outcome, it is by no means guaranteed. The new electoral law (“Rosatellum Bis”) combining a system of proportional representation (2/3 of seats) and first past-the-post (1/3 of seats) has also repealed the majority premium of 40% present previously, therefore this makes it harder to envisage an outright majority. In the probable scenario that the election does not reach a majority, in order to avoid having a new round of elections, the parties would be pressed to form a coalition government. A long period of negotiations would therefore be foreseeable, which would come alongside a period of political instability and lack of reforms.

The ranges of possible coalition governments see an alliance of the 5SM with the centre-left as they are relatively aligned in the political spectrum (see figure below). Also, the possibility of a Eurosceptical coalition is not unlikely, with the 5Star movement forming an alliance with the League and the Brothers of Italy. Finally, a government of grand coalition uniting the centre-right and centre-left coalition may be on the table – although the lack of cross points between the two alliances would make it a low probability event. It would also be hard to negotiate who would step forward as leader and to present a consistent policy agenda.

.PNG)

The likelihoods of the 5Star Movement to win an outright majority are slim but not impossible. Despite the recent reversals of the movement from its Eurosceptic origins, investors’ uncertainty could come from its ambiguous attitude towards the single currency. A depreciation of the euro, accompanied by an increase in government bond yields, is a likely implication if the 5SM wins.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum