Did Central Banks Cause The Last Financial Crisis? Will They Cause The Next?

Pub. Date

Pub. Date

Pub. Type

Pub. Type

Authors

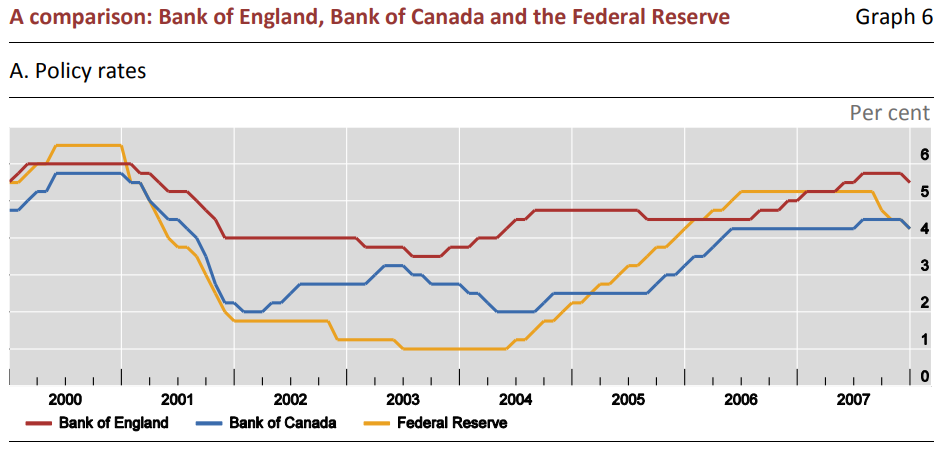

Recent history suggests that raising interest rates higher than warranted by macroeconomic prospects would not be the right policy for financial stability. The significant tightening of monetary policies in the advanced economies from mid-2004 to mid-2006 failed to stop increased risk-taking in the financial system. The pre-GFC policy failure was not lax monetary policy but the failure of regulators to address (and markets to sanction) new risks created by innovation in international banks. Post-crisis monetary expansion, inadequate at first but ultimately taking many radical forms, ended a severe global recession. It did so without increasing aggregate debt/income ratios of the non-financial private sector in the advanced economies. But it has increased the interest rate sensitivity of the balanced sheets of financial intermediaries, an effect magnified by new regulations. Accounting rules and prudential regulations, which do not treat interest rate risk well, need to be re-examined. Current macroprudential policies largely fail to address the increased exposures to interest rate and liquidity risks faced by financial firms. The problem for monetary policy is that, given the scale of interest rate risk on the balance sheets of financial intermediaries, the macroeconomic effects of interest rate increases have become larger and much more uncertain.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

The Nature of the Inflationary Surprise in Europe and the USA

21 Mar 2024

Discussion Papers

Energy and Climate Policy in a DSGE Model of the United Kingdom

08 Mar 2024

Discussion Papers

Exploring Alternative Data Sources for Household Wealth Statistics

24 Jan 2024

Discussion Papers

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum