The dilemmas facing central banks in the advanced economies

Recently NIESR raised its forecast for global output growth in 2017, to 3.6 from 3.3 per cent, mainly because of stronger than expected data on recent economic activity in a number of advanced and emerging market economies.

Authors

Recently NIESR raised its forecast for global output growth in 2017, to 3.6 from 3.3 per cent, mainly because of stronger than expected data on recent economic activity in a number of advanced and emerging market economies. But at this same time, NIESR lowered its inflation forecasts for 2017. These changes mirror a dilemma recently faced by central banks, especially in some key advanced economies. On the one hand, output and employment gaps have narrowed, with unemployment rates in some cases—such as the United States, Japan and Germany—indicating close-to-full employment. But on the other hand, actual and expected inflation have remained below targets and also wage increases have remained notably subdued.

In the US, the Fed in June raised interest rates again, arguing that recent below-target and declining inflation reflected transitory factors. The Bank of Canada also raised interest rates in July, despite below-target inflation, which it similarly attributed to temporary factors, on the grounds that ‘the economy is approaching full capacity’ so that inflation could be expected to rise to the target within a year.

When making such monetary policy decisions, central banks have to weigh at least three considerations: their confidence in their understanding of the determination of inflation, the credibility of their inflation targets in relation to inflation performance, and the relative costs of the policy mistakes that they risk.

With regard to the determination of inflation, recent experience has cast further doubt on Phillips Curve-type relationships between unemployment and inflation. Across many countries, inflation has recently been lower than past relationships with unemployment would have implied, and estimates of the NAIRU (the non-accelerating inflation rate of unemployment) have consequently been revised down. Thus, the mid-point of the Fed’s estimate of the longer-run unemployment rate consistent with its inflation target has been revised down in several steps from 5.6 per cent when it began inflation targeting in 2012 to 4.6 per cent in June 2017: see figure 1. Even now, with actual unemployment below 4.6 per cent, price inflation remains below target and has declined in recent months, and wage inflation has remained subdued. Further downward revisions in the Fed’s estimate of long-run normal unemployment may, therefore, well be on the way.

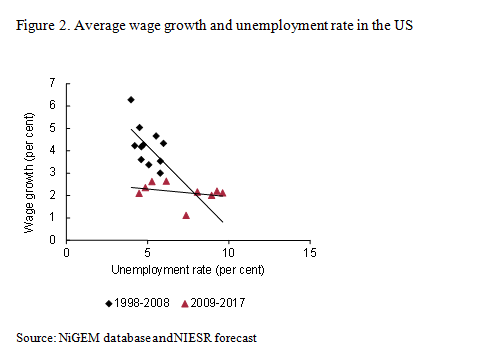

In fact, there is little sign of a significantly downward-sloping Phillips curve in recent unemployment and inflation data, as illustrated in figure 2. The relationship between unemployment and wage and price inflation may have changed for a number of reasons, including changes in the labour market that may have made the ‘headline’ unemployment rate less meaningful as a measure of the employment gap; effects of globalisation on competition and price formation; declines in the power of trade unions; and a downward shift and firmer anchoring of inflation expectations, perhaps resulting from inflation targeting or the Great Recession.

Turning to the credibility of inflation targets, the inflation targets of the central banks of the major advanced economies are meant to be symmetric, yet for many years inflation has been predominantly below target. In the US, for example, it’s been below target for almost the whole of the period since inflation targeting began in 2012. For an inflation target to be credibly symmetric, inflation should presumably be somewhat above target around cyclical peaks, when output is close to capacity, and below target during cyclical troughs. This implies that currently central banks can afford to be relatively relaxed about inflation rising above target to a limited extent in the short term, while they continue to aim for the target over the medium term.

Finally, central banks have to weigh the relative costs of the mistakes that they risk making. The costs of the risks in either direction seem significantly asymmetric. If a central bank tightens too late or too weakly, so that inflation rises inordinately above target, it can act promptly, and in principle it has unlimited ammunition to correct its mistake. But if the central bank tightens too soon or too strongly, not only will the scope for easing be more limited, given that interest rates are already low, and given the zero lower bound, but the economy could be unnecessarily weakened, with not only short-term costs in terms of lost output, income and employment, but long-term costs arising from losses of productive potential.

These considerations suggest first, that there are currently strong grounds for central banks to pay more attention in their deliberations to data on price and wage inflation, and on inflation expectations, than to data on unemployment and estimates of output gaps; second, that the credibility of their symmetric inflation targets is unlikely to be damaged if inflation is allowed to rise somewhat above targets in the short term in the period ahead; and third, that without clear evidence that actual or expected inflation is rising significantly above targets, central banks should approach with particular caution any decision to reduce accommodation.

Related Blog Posts

Related Projects

Related News

Call for Papers: Lessons From Quantitative Easing & Quantitative Tightening

09 Feb 2024

1 min read

Related Publications

Inflation Differentials Among European Monetary Union Countries: An Empirical Evaluation With Structural Breaks

20 Nov 2023

National Institute Economic Review

The Macroeconomic Effects of Re-applying the EU Fiscal Rules

20 Nov 2023

National Institute Economic Review

Another Look at a Sensible Fiscal Policy for the Sharp Rise in Government Debt

20 Nov 2023

National Institute Economic Review

Monetary Policy: Prices versus Quantities

20 Nov 2023

National Institute Economic Review

Related events

Assessing Cycles and Structural Changes in Markets

Business Conditions Forum