Authors

Key points

- Global economic activity has rebounded from the sharp fall in the first half of last year. But the continuation and pace of the global recovery are highly dependent on the evolution of the virus and the coverage of vaccinations.

- A strong and sustained global economic recovery depends on controlling the virus. The number of virus cases globally continues to increase and the global number of deaths has surpassed 3 million. Vaccines have come on stream faster than expected a year ago. They offer the prospect of control of the spread of the virus, a reduction in the number of additional deaths, and a return towards ‘normality’ in social and economic life. However, the emergence of new variants of the virus raises an important risk to the economic recovery if the vaccines are less effective against them. Continued waves of the virus and the re-imposition of restrictions could occur.

- In recent months, the unexpectedly rapid development of vaccines against Covid-19 and the programmes of vaccinations have provided a boost to confidence and economic activity. The pace of vaccination has, however, been uneven across countries, with emerging economies running well behind advanced economies, creating an increased need for an international effort to ensure that vaccinations are widespread, enabling maximum benefits to be gained.

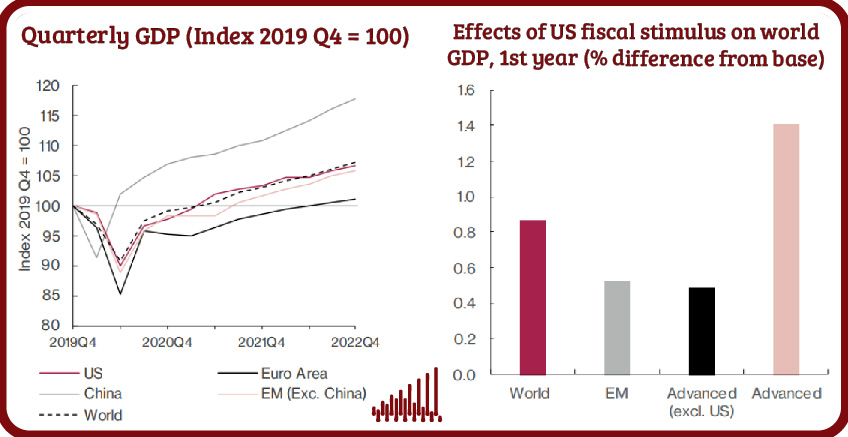

- Another important recent development has been the American Rescue Plan – a $1.9 trillion (about 9 per cent of GDP) fiscal boost to the US economy. This stimulus will boost US and global GDP growth this year, as well as provide some support should there be retrograde steps due to the spread of the virus.

- Following these developments, we have raised our forecast for global GDP growth this year from 4½ per cent to 5½ per cent. For 2022, we now project GDP growth of 4¼ per cent (up from 3¾ per cent)

- The pace of economic recovery will differ across economies. GDP in the US is now expected to reach its prepandemic level this year, while GDP in the Euro Area is forecast to remain below its pre-pandemic level until late 2022. In contrast, GDP in China is already 8 per cent above its level at the end of 2019.

- The pandemic has led to GDP being lower than anticipated. We estimate that the pandemic will result in the level of global GDP being around $6½ trillion (about 4 per cent of GDP) lower in 2025 than our pre-pandemic expectation, with the cumulative loss of GDP up to 2025 amounting to around $36 trillion.

- One legacy from the pandemic has been higher public debt, with debt to GDP ratios in advanced economies having risen by around 15 – 20 percentage points, equivalent to around $7 trillion. With low government bond yields, the level of increased debt appears not to be a major immediate policy concern, but it does create a vulnerability to both higher interest rates and further adverse shocks that would require a response in the form of higher government borrowing.

Related Blog Posts

Related Projects

Related News

news

Why it’s not worth worrying that the UK has technically entered a recession

26 Feb 2024

4 min read

Related Publications

publication

Recessionary Pressures Receding in the Rearview Mirror as UK Economy Gains Momentum

12 Apr 2024

GDP Trackers

Related events

Summer 2023 Economic Forum

11:00 to 12:00

11 August, 2023

Spring 2023 Economic Forum

11:00 to 12:00

12 May, 2023

Winter 2023 Economic Forum

11:00 to 12:00

10 February, 2023

Autumn 2022 Economic Forum

11:30 to 12:30

18 November, 2022

Summer 2022 Economic Forum

11:00 to 12:00

5 August, 2022

Spring 2022 Economic Forum

11:00 to 12:00

13 May, 2022

Winter 2022 Economic Forum

11:00 to 12:00

11 February, 2022

Autumn 2021 Economic Forum

11:00 to 12:00

12 November, 2021